Like many busy appraisers, I can spend a lot of time in my own little world just trying to keep my head above water. Trying to meet deadlines, keep my clients informed, and put out a quality product in this busy market is enough to make my head spin. Lately, though, I’ve been trying to carve out some extra time to find out about what other appraisers are saying and doing in this unusual market.

I’ve been consuming more news articles, blogs, and podcasts than ever before, but there are always some questions that never seem to get answered. I started to think about the best way to approach those questions, and in doing so I became reacquainted with a useful tool in statistics…the bell curve.

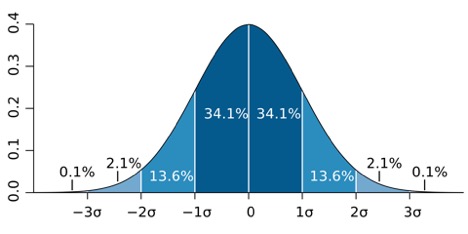

The bell curve is the informal name for a normal (or Gaussian) distribution. You may recognize this from an otherwise long-forgotten class in math or statistics, but you may not recognize its applicability to appraisal. You see, a bell curve is a way to demonstrate probability, and probability is a very important concept for appraisers. Fannie Mae defines market value in part as “the most probable price that a property should bring…” Thus, probability is the very foundation of the most common definition of market value.

The bell curve is the informal name for a normal (or Gaussian) distribution. You may recognize this from an otherwise long-forgotten class in math or statistics, but you may not recognize its applicability to appraisal. You see, a bell curve is a way to demonstrate probability, and probability is a very important concept for appraisers. Fannie Mae defines market value in part as “the most probable price that a property should bring…” Thus, probability is the very foundation of the most common definition of market value.

Let me summarize the theory of a normal distribution. The peak of the curve represents the central tendency of a distribution of random variables (in a normal distribution, the mean, median, and mode are all represented by the peak). Each section of the distribution above represents the probability of a random variable falling within each multiple of a standard deviation from the mean. If I’m starting to lose you at this point, stick with me. It will become much clearer when we get to some real-world experiences and applications.

So this brings me back to my real-world unanswered questions. While I’d like to address several questions, today I’ll just deal with one: What is the explanation for the ‘appraisal gap?” In other words, why are appraiser estimating market value below the contract price so often?

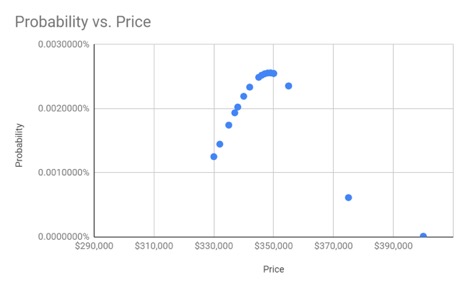

My answer to this question came through an unlikely source…a listing agent attempting to convince me that I should appraise a property for the purchase price. She had a mountain of offers and sent me a spreadsheet of them once she had obtained the ‘highest and best’ from all the potential buyers. I have simplified the data somewhat, but the summary is as follows:

Knowing that there were multiple offers and given the increasing market, most of the buyers were willing to pay above the asking price of $330,000 (which was a pretty reasonable price based on the sales in the neighborhood). The average offer was a little over $348,000, but the highest offer was $400,000. As you can see in the histogram above, the vast majority of the offers fell within the $340,000 to $350,000 price range. If plotted on a normal distribution (and before you say it, I know that all distributions aren’t ‘normal,’ including the one above, which I will address in the future), the offers look like this:

The peak of the curve is just under $350,000 (as expected just glancing at the histogram). This marks the most probable price of an additional random variable being added to the distribution. In this case, the additional random variable would be the next ‘highest and best’ offer received by the listing agent. When the agent receives the next offer, the highest probability is that the offer will be something close to $350,000. But what offer will the seller accept $400,000.

Herein lies the appraisal gap. The definition of market value is consistent with the top of the curve, whereas in the environment of multiple offers, the actual contract price will be represented by the offer which is the statistical outlier. At this point, it is necessary to switch from statistics to economics and psychology to answer the next question…’why.’

Many will say, we have a willing buyer and seller, so we have an indication of value. This is true, but the value of what. The motivation of the seller is obvious. Of course, you would accept the highest offer from a buyer who you think will actually make it to the closing table. The motivation of the buyer is a different story. Why would the buyer be willing to pay $70,000 more than the asking price? What were they paying for? I’ve heard about the motivations of quite a few different buyers at this point. There are many different motivations, but there are a few common themes:

- Time – It takes time to find a house. Time to make an offer. People have lives and want to get back to living them after finding a house. After losing out on bids for other properties, many buyers decide that there is a value in not wasting more time. For an out-of-state buyer, there is a value in not having to make another potentially expensive trip to look at more houses.

- Expectations – Expectations are the self-fulfilling prophecies of economics. The perceived expectations of future events have a present value, even if those events don’t happen. If buyers’ expectations are that interest rates will rise, then there may be a willingness to pay more to lock in to a low rate now, even if they will end up paying a premium in the present for perceived savings in the future. It is a self-fulfilling prophecy, as the buyer is paying an interest rate premium in the present that hasn’t yet been earned.

- Uncertainty – Uncertainty and expectations go hand-in-hand. Markets hate uncertainty. It creates volatility, as the number of expectations priced into the current market is high. Think in terms of insurance. The insurance premium is the present value of the level of risk and uncertainty.

- Competitiveness – People like to win. It may be unconscious (and even if it is conscious, many wouldn’t admit it), but there is a value to being the winning bid.

There are many more motivations, some specific to a particular buyer alone, and many which are common to all buyers. The mix of motivations and magnitude of each is critical to evaluating the difference between price and value. The one thing common to each of these motivations is that they are not real estate. If a buyer pays a $10,000 premium to win the bid, that $10,000 represents something that cannot be resold. In fact, none of the motivations that I mentioned are intrinsic to real estate itself. None can be resold, although many may be replicated in future buyers, depending on what factors in the market are working to shift supply and demand.

In my example, the typically motivated buyer in the market was willing to pay approximately $20,000 above the asking price. The atypically motivated buyer was willing to pay $70,000 above the asking price. That $50,000 difference is inconsistent with the definition of market value, which assumes that both parties to the transaction are “acting prudently, knowledgeably, and [assumes] that the price is not affected by undue stimulus.” There is also the assumption that both parties are “typically motivated…well informed or well advised” and are also acting in their “own best interest.” The $50,000 difference simply doesn’t meet that test.

It should be of note to any lender out there, that the underpinnings of demand (even represented by the typically motivated buyer) can be tenuous in these changing market conditions. Artificially low interest rates were a significant proportion of the increase in prices during the past year. When monetary policy changes, so does the proportion of the price that was impacted by the increase in purchasing power and the impact of expectations of future rates on current pricing.

For the appraisers reading this article, there are a lot of implications with regards to how you evaluate comparables, and in particular how you reconcile them. The next article will answer the question, how do I reconcile comparables with a wide range of adjusted sales prices?

Have any comments or would you like to submit content of your own? email comments@appraisalbuzz.com.

Share this article

Written by : Brent Bowen

Brent is the president of Texas Valuation Professionals, Inc. (www.txvaluepro.com) in Plano, Texas and has been appraising residential real estate in north Texas for 25 years. He graduated from Baylor University with an enthusiasm for both economics and real estate, which made real estate appraisal a perfect fit. Rarely satisfied with the status quo, Brent hopes to always be open to further development, both professionally and personally.

4 Comments

Comments are closed.

Thank you for explaining a nice method to determine “the most probable price (specifically, in a rapidly appreciating market) which a property should bring in a competitive and open market…” It looks like a terrific way to analyze a Purchase and Sales Agreement. I will now start asking Listing Agents for details regarding multiple offers received and creating spreadsheets and probability graphs for our clients’ reference. My question is: How can an appraiser adjust for discounting a recent comparable closed sale with a sales price that was much higher than “most probable price” if it is now considered a true market (comparable) sale but was deemed an outlier by Fannie Mae’s “Definition of Market Value” before it closed? Instead of providing a single point value opinion in reports, perhaps a range of value in a rapidly appreciating (or declining) market “probably” would be the most reliable and credible value conclusion an appraiser can provide to a client? Then the client can decide on a property’s collateral value they are willing to lend on, and not the appraiser. Lenders would be better served if they relied more on their senior underwriters for a final, final value opinion to determine the LTV ratio. The probability of the truth of a property’s current market value would be improved. But, seriously, thanks for the information in your article, and good luck to all of you participating in valuations during these bizarre residential market times.

Bill,

Thanks for your kind feedback. Some of these issues will be addressed in part 2, which I am working on right now. I find that once you understand the concept, you will be able to see the outliers in your data without ever having to plot them. Half of the battle is understanding the concept. The other half is knowing what to do once you recognize a statistical outlier in your distribution. This impacts comparable selection, reconciliation, and even the process of deriving and supporting adjustments. I’ll delve into those areas more deeply in future articles. Thanks!

Brent, I’m not sure you picked the right event to analyze. Market value is the most probable price, not the most probable offer. The event – the dice roll – is the marketing of a particular property – so that if the same or similar property were sold 100 times, $X would be the price that the property would fetch, on average. Sometimes the price would be extraordinarily high, others extraordinarily low. Instead, the dice roll you used is the offer of each particular buyer. It’s obvious that the most motivated buyer always, always sets the price and gets the property.

The appraiser must decide whether the most motivated buyer fairly represents a type of buyer who would likely be in the mix for any marketing effort for that property type. To take a hypothetical from Seattle, our high bidders are often tech workers with 6-figure salaries. We haven’t run out of them yet. They may be the high buyer in most transactions. They get the house and set the market. Why would we call them “outliers” just because others with fewer resources bid lower?

One phrase you used pricked my ears: “none of the motivations that I mentioned are intrinsic to real estate itself.” The idea of intrinsic asset value has a long history, but that’s not the direction of appraisal and asset valuation in the last few decades. Prices arise from behavior, and behavior arises from motivations. To say, “this motivation is kosher for market value but that one is not,” needs a lot more justification than to be tossed off as if everyone agrees on what that means.

Vince,

I just saw your comment for the first time today.

Your comments highlight something that was a concern when I decided to take on such a large topic in a condensed format. I’m working on expanding this beyond the information presented in this 3 article series, which I think might be more helpful for someone like yourself who is digging below my brief introduction to these concepts. You asked some great questions which deserve much more time than the few hundred words that I had to work with.

While I agree that the concept of intrinsic value has taken a backseat to that of a point-in-time prediction of price, I think that has been at the detriment to the lending community. The last mortgage meltdown made that abundantly clear. However, at its core I think that the FNMA definition of market value itself attempts to lead the appraiser toward the consideration of intrinsic value. Hopefully we can connect in the future and discuss these ideas further. I appreciate your input!