The topic of inflation has dominated the news cycle lately. Let’s put aside for the moment the causes of the steadily increasing rate of inflation, and instead take a closer look at what impact it has on housing prices.

Let me preface this by saying I don’t have a crystal ball (or a Delorean) so I can’t tell you what the future holds for residential real estate. here are multiple factors at play in the supply and demand for housing which often have contradictory effects. Be that as it may, inflation does add some new variables to that equation that are worth noting.

First, let’s talk about effective demand. There are a lot of people who want homes right now, but what counts is the willing and able buyer. We will discuss this ability in terms of buying power.

Interest Rates

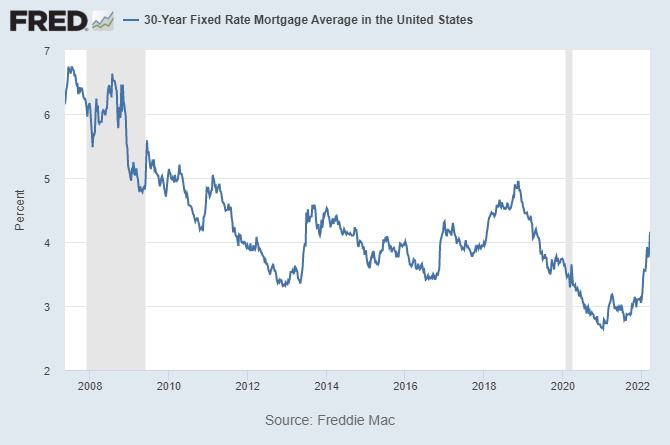

In order to deal with inflation, the Fed has planned, and already implemented, some changes in monetary policy. These policy changes will correlate to some significant changes in interest rates. This graph shows the changes in the interest rate for 30 year mortgages (which are already a full percentage point higher than they were at the beginning of the year).

Freddie Mac, 30-Year Fixed Rate Mortgage Average in the United States [MORTGAGE30US], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/MORTGAGE30US, March 17, 2022.

The increased rates have a significant impact on buying power. Consider this example:

A buyer is evaluating the purchase of a home priced at $625,000. If the buyer is making a 20% down payment ($125,000), the loan amount would be $500,000. If the buyer is able to get an interest rate of 3%, the resulting mortgage payment would be $2,108 per month. The buyer thinks they can make that payment, but decides to wait another year. What happens if inflation strikes and interest rates are 5% next year? In order to achieve that same payment of $2108 with 5% interest, the loan amount would have to be $392,600. Even if the buyer decides to keep the same down payment the house price would have to be $517,600 for the buyer to afford the same home. That would reflect a necessary price reduction of 17% in order to account for the loss in effective demand for that buyer.

That puts history into a little bit of perspective. Glance back at that interest rate graph and you can see that the drop in interest rates between 2019 and 2021 resulted in exactly the reverse scenario described in the example above. The drop of interest rates from the high 4% range to the high 2% range accounts for a significant portion of the historic growth in home prices during the past 2 years.

Consumer Prices

The interest rate effect isn’t the only factor related to inflation that impacts effective demand. Let’s consider the rest of the budget for our example buyer. According to HUD estimates, the national median family income in 2021 was 1.7% higher than 2020. Good news! A little more money in the pocket for our buyer…but what about their expenses. As of February 2022 the inflation rate (Consumer Price Index) was reported at 7.9%. Thus, while this buyer has a bit more income, they lost a lot of ground when it comes to expenses. This increase in expenses means that this buyer is going to have a harder time making that monthly payment. It is not unreasonable to deduce that some of the money they had budgeted for a house payment will probably end up getting pumped into their gas tank, or spent on any of a hundred other things on their next credit card bill. This has a direct impact on buying power.

At this point you might be thinking, “Oh no, we are headed for a market crash!”

Mitigating factors

Of course there are other forces at play when it comes to inflation. Remember effective demand involves a willing and able buyer. High inflation creates an incentive not to hold cash. In an inflationary cycle holding cash is a losing game. Every day that same dollar will be able to buy less. The incentive is therefore to transfer cash into hard assets, like real estate. There are also demographic changes in our population (primarily the population bulge of millennials at the prime home buying age) that have impacted the overall demand for real estate.

Lest we forget, demand is only half of the equation. The supply of housing remains historically low. If a decrease in demand results in 10 competing offers instead of 20, there may not be a significant difference in the resulting price.

Looking ahead

While nobody knows what the future holds, inflation has happened before. For those of us who weren’t born yet or weren’t old enough to be watching the news in the 1970s when inflation hit double digits, it might be worth your time to do a little research. I recently stumbled upon Money Mischief: Episodes in Monetary History by Milton Friedman. The book has some excellent analysis of inflation that I have found very interesting. Inflation will eventually impact the national debt, tax rates, government spending, and the output of the economy as a whole (GDP). I recommend that we all become more informed and remain aware in this ever changing world. As the saying goes, “Those who cannot remember the past are condemned to repeat it.”

Share this article

Written by : Brent Bowen

Brent is the president of Texas Valuation Professionals, Inc. (www.txvaluepro.com) in Plano, Texas and has been appraising residential real estate in north Texas for 25 years. He graduated from Baylor University with an enthusiasm for both economics and real estate, which made real estate appraisal a perfect fit. Rarely satisfied with the status quo, Brent hopes to always be open to further development, both professionally and personally.

4 Comments

Comments are closed.

An important thing left out of this article is wage inflation is also occurring which has a big impact on demand/affordability just like interest rates.

Wage inflation was referenced in the article. It was reported by the measure of national median family income. The point was made that wage inflation is lagging behind the inflation of goods and services, which erodes buying power.

“Those who cannot remember the past are condemned to repeat it.”

EXACTLY what I told friends, family, and colleagues in 1987, 1999, and 2005.

And now~

[…] impact of increasing interest rates and inflation on the residential real estate market. In that article I demonstrated the decrease in buying power from rising interest rates. That decrease in buying […]