Imagine standing before a beautifully decorated Christmas tree, ready to flip the switch. You plug in the lights and nothing happens. You check the plug, the length of the wire and each bulb, one at a time, until you find that one tiny bulb somewhere along the strand is broken or loose, and its causing the entire string of lights from working.

Similarly, in complex systems, the weakest link often determines how well the system functions or whether the system functions at all. The upcoming mandate for the Uniform Appraisal Dataset 3.6 (UAD 3.6) and the redesigned Uniform Residential Appraisal Report (URAR) is such a system. If any single stakeholder in the mortgage/valuation chain fails to support the standard, the entire “string” of appraisal-to-loan delivery can go dark.

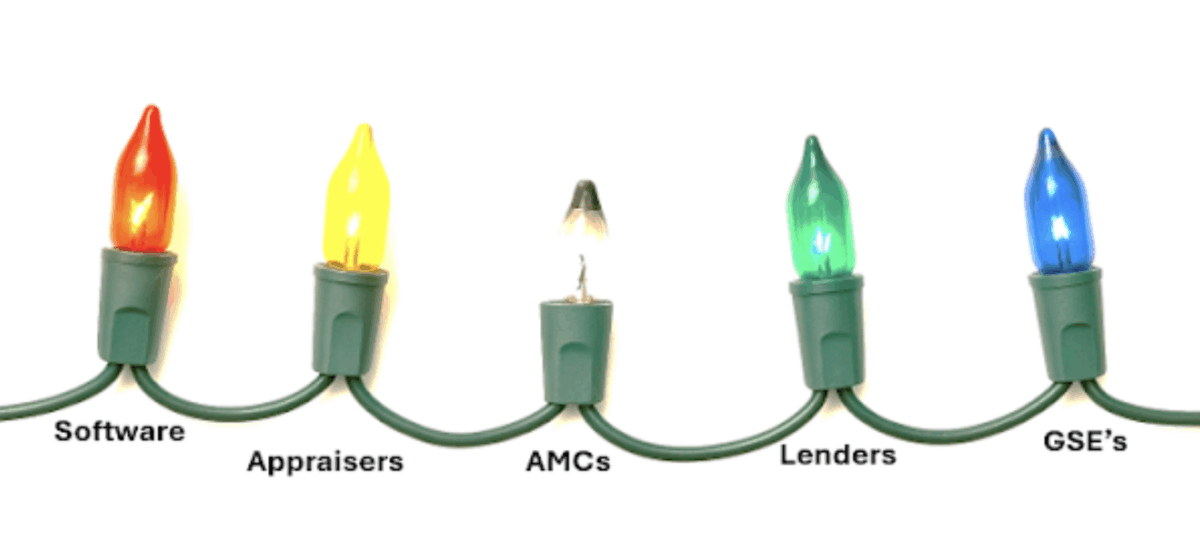

That’s why appraisal software, appraisers, appraisal management companies, lenders and even the GSEs, must all be certified and/or ready to go for UAD 3.6 to work as intended.

This image illustrates what’s at stake as the mortgage and valuation industries move toward the mandatory implementation of the UAD 3.6 and the redesigned Uniform Residential Appraisal Report (URAR) on November 2, 2026.

UAD 3.6 represents the most sweeping modernization of appraisal data and reporting since 2005 when the “1004 Appraisal Form” was last redesigned. It is intended to improve accuracy, consistency, and digital integration across all aspects of the valuation and mortgage ecosystem.

But the new standard will only succeed if every link in the chain – appraisers, appraisal software vendors, AMCs, lenders, and of course, Fannie Mae and Freddie Mac – are ready. If even just one segment lags behind, or isn’t ready, the lights won’t come on.

Good Intentions

The intent behind UAD 3.6 is sound. The GSEs envision a future where every appraisal report flows through a standardized data structure, allowing automated checks for completeness, consistency, and reasonableness. This improves quality control, speeds up underwriting, and reduces repurchase risk. All good things for everyone involved.

For lenders, this hopefully means fewer delays and cleaner first time submissions. For AMCs and appraisal technology providers, it promises streamlined operations and transparency. And for appraisers, it’s an opportunity to be recognized not just as form fillers or report writers but as data professionals in an evolving digital mortgage process.

But this transformation requires total synchronization. UAD 3.6 isn’t simply a new “form.” It’s like an entirely new language and every participant must speak it fluently, from the moment an appraisal order is created to the moment the report is submitted to the GSE portal.

That undeniable interdependence is precisely why partial readiness won’t work. The system only functions when every “bulb” is working in unison.

Why Universal Readiness Matters

The valuation process works like a relay race. Orders pass from lender to AMC, from AMC to appraiser, and from appraiser through multiple layers of review before final delivery. If any handoff falters, the baton is dropped.

- If appraisers aren’t ready, they can’t deliver the new report format. Orders pile up, closing dates are missed, and lenders can’t originate loans using appraisals.

- If appraisal software vendors aren’t ready, appraisers can’t produce compliant reports.

- If AMCs aren’t ready, they can’t order, receive, review or transmit those reports.

- If lenders aren’t ready, they can’t submit them to the GSEs.

- And if the GSEs’ delivery portals are ready but the data isn’t clean, everything stops at the gate.

- And what about VA, FHA and USDA or Non-QM?

Like that string of Christmas lights, one dark bulb cancels out all the bright ones. Success requires 100% complete alignment, not majority compliance.

Appraisers at the Center

Every modernization effort in mortgage lending eventually comes down to people. And appraisers sit at the center of this one – again.

Even if every system upstream and downstream is certified or ready for UAD 3.6, the entire process begins with the professional boots on the ground inspecting the property and completing the report. If appraisers aren’t trained, equipped, or willing to adopt the new framework, no amount of readiness elsewhere will matter.

There’s a risk that many appraisers, especially the older and more rural appraisers, may resist the transition. Some appraisers may see it as just another thing imposed on a profession that has absolutely nothing to do with determining the value of a property. Others may hesitate to invest time and money in new tools like mobile applications, lidar equipped phones and new data streams before they see broad lender demand.

This reluctance could create a bottleneck just as lenders and AMCs are gearing up for compliance. If the “supply side” of the appraisal equation isn’t ready, even the most advanced technology platforms and the most compliant lenders will find themselves stuck without appraisers willing and able to complete the assignments.

The Partial-Readiness Problem

Let’s imagine it’s this time next year, just prior to the mandate of November 2, 2026. One major mortgage lenders systems are live and ready to receive UAD 3.6-compliant reports. Loan officers, reviewers, audit teams and others are all trained and ready to go! Its preferred AMC is also ready, as is the appraisal management platform it uses. Several appraisal software companies have proudly announced their certification and are also ready.

Everything should be ready for liftoff, except that perhaps a large share of independent appraisers have not yet adopted the new version of their software, or they haven’t completed any continuing education to inform them of the new process/form. They are still producing appraisals in the old 2.6 format.

What happens then?

- The lender sends out appraisal orders requiring UAD 3.6 delivery, but many appraisers decline or delay.

- AMCs scramble to find qualified appraisers who can accept the orders in the geography of the property.

- Turn times double or triple, especially in rural markets or for specialized properties.

- Borrowers grow frustrated, loan pipelines clog, and closings are delayed or scuttled.

- Lenders start requesting exceptions or extensions in the mandate, pleading for more time.

- The GSEs, under pressure, may be forced to consider limited waivers or temporary dual acceptance of old and new formats, compromising the clean transition the industry has been working toward.

The bottom line? Even if 90% of the industry is ready, the 10% that isn’t, can bring the entire process to a halt. Every bulb matters!

The Stakes for the Industry

UAD 3.6 is not just another form update, it’s an inflection point. How the industry handles it will signal whether we can modernize collaboratively or whether we’ll repeat the fragmented transitions of the past. Appraisers must recognize they have many clients and their requests are changing.

Lighting the Whole Strand: What Must Happen Now

With just over a year before limited production begins and a little more than a year before full enforcement, the industry still has time, but not much. The path forward demands collective action.

- Education and communication: Appraisers need clear, non-technical education on what UAD 3.6 means for their daily workflow, not just regulatory jargon. This is widely available today through appraisal education companies. Appraisers, AMC employees and lenders need to become aware, educated and ready.

- Shared responsibility: Lenders, AMCs, and software vendors must see appraiser readiness as a shared problem and one that requires a shared investment in order to be ready.

- Be creative! Offer incentives for early adopters: Early certification programs, priority placement, or premium assignments can motivate appraisers to act sooner rather than later.

- Cooperation and coordination, not competition: Embrace “coopetition.” This transition isn’t about who gets there first. It’s about ensuring everyone arrives at the same time.

The key word is together: A single bulb shining in isolation doesn’t light a tree. The power of the system lies in its connection. If one link breaks, it won’t just be an inconvenience.

On November 2, 2026, the industry will flip the switch. The question is whether we’ll see a brilliant, fully illuminated system or a dark strand with a few glowing sections and a lot of frustration in between.

The choice is ours. Let’s make sure every bulb lights and shines brightly!

Share this article

Written by : Tony Pistilli

As President of Valuations at Restb, Tony Pistilli is responsible for providing direction to the application of Restb.ai's products and services for the valuation segment of the real estate industry, working with the product team to develop and expand the suite of offerings and prioritizing development initiatives. Tony also plays a vital role in expanding Restb.ai's reach in the valuation and appraisal industry, as well as fostering relationships with lenders and related industry partners.

Tony has over 30 years of executive-level real estate valuation and lending experience including working with national banks, mortgage companies, federal agencies, and leading appraisal management firms. He is a certified residential real estate appraiser in Texas and is an AQB Certified USPAP Instructor. In 2011, he was the first recipient of the Valuation Visionary Award presented by the Collateral Risk Network at Valuation Expo.