There seems to be a consensus among appraisal reviewers that the appraiser should not average the adjusted sales prices of their comparables in order to arrive at an indicated value of the subject from the Sales Comparison Approach. Fannie Mae is referenced as the source of this prohibition, although no such prohibition explicitly exists according to Fannie Mae’s Selling Guide.

There is a prohibition on averaging techniques, but that applies in the Reconciliation section with regards to reconciling the three approaches to value. In other words, Fannie Mae does not want you averaging the indicated values from the Sales Comparison Approach, Cost Approach, and Income Approach in order to arrive at an opinion of value. The discussion of the reconciliation of the indicated value of each comparable sale contains no such prohibition. Instead, this section states:

“…the appraiser’s comments must reflect his or her reconciliation of the adjusted (or indicated) values for the comparable sales and identify why the sale(s) were given the most weight in arriving at the indicated value for the subject property.” (Fannie Mae Selling Guide, B4-1.3-09)

I think a solid case can be made for identifying all comparable sales as being worthy of equal weight (with one significant caveat I’ll address in a moment). In short, I’m suggesting that the mean may be the best way to reconcile those sales.

Why can I make such a bold claim without even looking at a single comparable? Because, that claim is what is consistent with Fannie Mae’s definition of market value.

“Market value is the most probable price that a property should bring in a competitive and open market…” (Fannie Mae Selling Guide, B4-1.101, emphasis added)

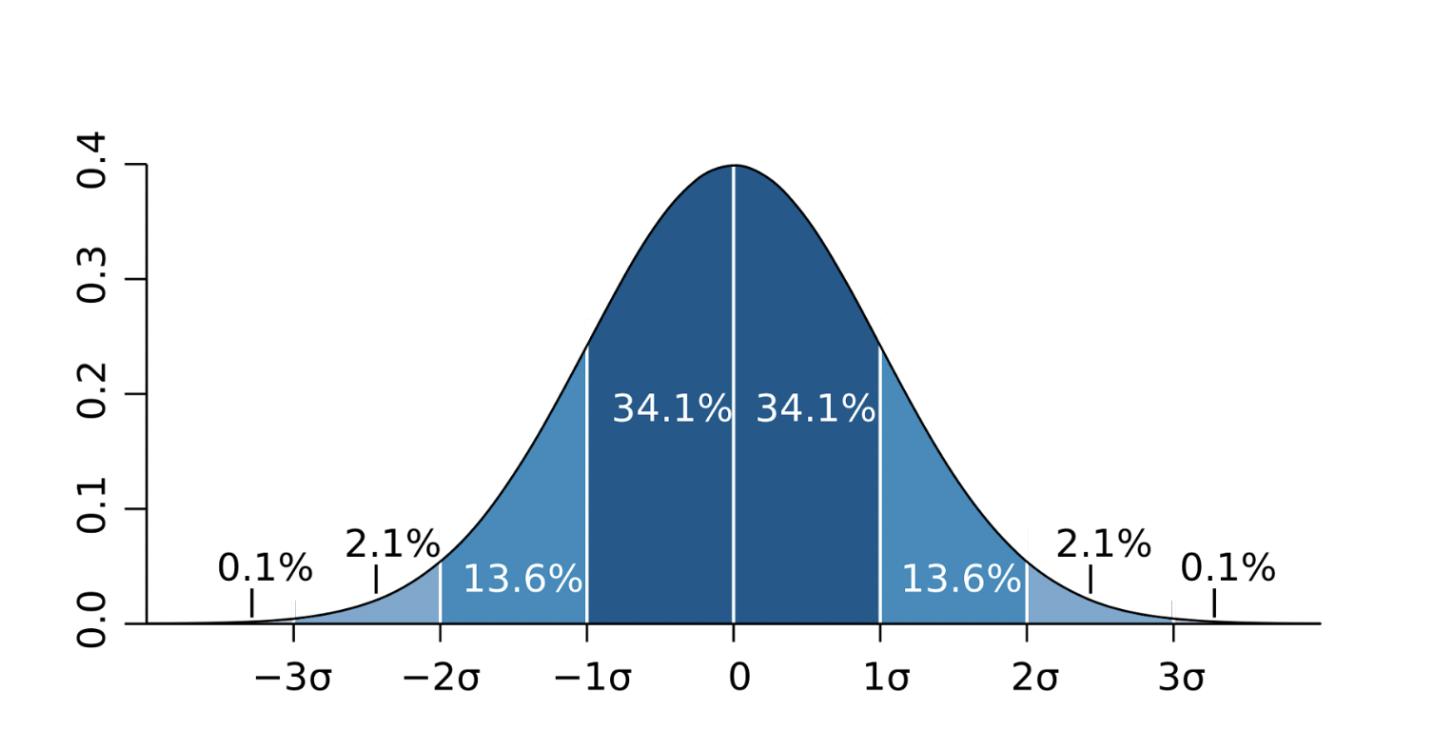

Since we are aiming for the most probable price, we are entering the world of probability distributions (aka, bell curves).

In a normal distribution, the most probable value is the mean. Now, to be fair, the median and mode are also synonymous with the most probable value in a normal distribution. Which brings me to my caveat…if your distribution (range of adjusted sales prices) is skewed, then the outliers must be removed so that the mean does not to reflect that skew.

The conventional wisdom is that the most similar comparable be given the most weight. But that begs a question…similar how? We can fairly easily observe the comparable which is the most physically similar, but what about the one that is the most transactionally similar? In other words, which comparable deviates the least from the mean? When I say ‘transactionally similar’ I’m not just referring to whether or not it is an arms-length sale. Transactional similarity refers to a transaction where the buyer and seller behave in a way that is most representative of the market, and thus the definition of market value. That is very difficult to observe in isolation. Observing that deviation requires context. In other words, where is that comparable sale in the distribution relative to the other adjusted sales prices in your data set?

(As an aside, it can be tempting to put a lot of weight on that ‘perfect’ comp, but don’t neglect the concept of transactional similarity. If you are taking a single sale and using it to justify adjustments and then weighing it heavily in your reconciliation, you are just building an appraisal around a single sale. That is bad appraisal practice, one which is ripe for abuse and manipulation.)

Once your market supported adjustments have been made (remembering that Fannie Mae requires adjustments for differences that impact value), the role of physical similarity should end. The adjustments process, when properly done, has equalized the comparables with regards to physical similarity. The reconciliation then becomes a time to view your data in context and consider transactional similarity. It would be perfectly reasonable, even good appraisal practice, to use a comment similar to this:

“Sales 2 and 4 were given the most weight as they were closest to the mean and thus considered the most transactionally similar and thus most reflective of the definition of market value.”

Whether you agree or disagree with my perspective on how to apply this in practice, the concept is one which has implications far beyond the details of reconciliation calculations. It is a piece of the puzzle of data collection and interpretation and in the overall development of a credible and reliable appraisal. In ‘Creating Formulas That Work’ I link this concept with many other puzzle pieces from various disciplines to create a powerful technique which will be transformative to your appraisal practice. Join us for this live class via Zoom on Monday, December 11th. It will be 7 hours of CE unlike any you’ve taken before.

Share this article

Written by : Brent Bowen

Brent is the president of Texas Valuation Professionals, Inc. (www.txvaluepro.com) in Plano, Texas and has been appraising residential real estate in north Texas for 25 years. He graduated from Baylor University with an enthusiasm for both economics and real estate, which made real estate appraisal a perfect fit. Rarely satisfied with the status quo, Brent hopes to always be open to further development, both professionally and personally.