On Thursday, August 27, Fed Chair Jerome Powell announced a new strategy designed to keep interest rates exceptionally low for a longer time.

This announcement turns William McChesney Martin’s punch bowl metaphor of 65 years ago on its head. In a 1955 speech, this former Fed chair described the Fed as a “chaperone who has ordered the punch bowl be removed just when the party was really warming up.” He had earlier noted: “In the field of monetary and credit policy, precautionary action to prevent inflationary excesses is bound to have some onerous effects. Those who have the task of making such policy don’t expect you to applaud.”

Powell’s Fed has determined that inflation is now so benign that it no longer needs to raise interest rates as a precautionary action against inflationary excesses. Yet, we have been feeling such excesses in capital assets, such as stocks and homes, for some time, and markets are applauding. This is perfectly foreseeable as lower interest rates get capitalized into higher asset prices.

By encouraging speculative pressures to enter into property valuations, the Fed is enhancing credit risks to lenders and borrowers alike. Perhaps, Fed members should also reacquaint themselves with another longtime Fed chair’s observations in 1947 about housing finance and inflation and the dangers of easy credit.

- A large proportion of recent loans have been made for a very high percentage of current sale price, which is greatly inflated.

- A large number of families of moderate and low income have been encouraged to assume mortgage debt that will be beyond their means when the present inflationary period is over, and is becoming increasingly burdensome as the cost of living goes up. Sellers and builders of houses have been enabled to make exorbitant profits. The Government has assumed and continues to assume contingent liabilities of great proportions.

- Easy credit has greatly increased the effective demand for both old and new housing far beyond the supply and this has greatly inflated prices.

- An increasing number of families are being priced out of the market now, in spite of the extremely easy financing terms, even though their need for housing is very great.

- There is no such thing as easy credit — It is easy to get into debt, but the easier it is to get in, the harder it is to get out.

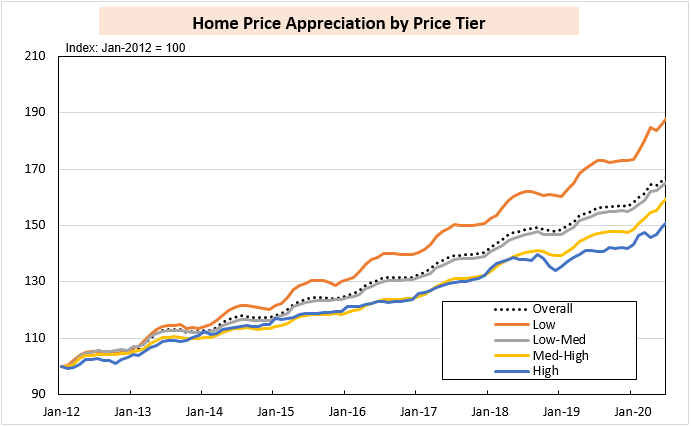

As demonstrated by the chart below, easy credit has fueled a housing boom since 2012, especially for the low price tier:

Note: Data for July 2020 are preliminary. Price tiers are set at the metro level and are defined as follows – Low: all sales at or below the 40th percentile of FHA sales prices; Low-Medium: all sales at or below the 80th percentile of FHA sales prices; Medium-High: all sales at or below the 125% of the GSE loan limit; and High: all other sales. HPAs are smoothed around the times of FHFA loan limit changes.

Source: AEI Housing Center, www.AEI.org/housing.

Given the inflationary effect of the Fed’s strategy, is it, as described in the media, a boon to those buying a home? Of course, what is “seen” is the lower monthly payment due to the lower rate. But “unseen” is the resulting increase in demand. And “foreseeable” is the higher home price resulting from increased demand operating against a constrained supply—we are in the midst of the strongest seller’s market since 2005 . A hat tip to Frédéric Bastiat, whose “That which is seen, and that which is not seen” was published in 1850.

To determine whether this is a boon for home buyers, consideration must be given to the impact of the Fed’s actions on home prices. The AEI Housing Center’s data indicate that Home Price Appreciation (HPA) has accelerated from about 6.6% in January 2020 to a projected 11.4% in August, an increase of 5 percentage points.

Source: AEI Housing Center, www.AEI.org/housing

HPA is projected to have been even stronger for entry level buyers—an increase of 6 percentage points since January.

Back in January, mortgage rates were 3.75% and today they are 3%. Spoiler alert: the payment drop due to the lower mortgage rate is more than offset by the impact of the higher home price on principal, interest, mortgage insurance premiums, property taxes, homeowners insurance, and closing costs, since all of these are related to home price and mortgage amount. The chart below displays the complete picture for a home purchased for $200,000 in January, and for one in August for $212,000, reflecting the home price increase due to the Fed’s actions.

*Adjusted upward by 6% to reflect the increase in home price due to the Fed’s actions.

Bottom line, an entry level buyer is now paying $4/month more when taking all effects into account, not saving $31/month when just looking at monthly principal and interest.

Lesson: Beware of the Fed bearing gifts.

Have any comments or would you like to submit content of your own? Email comments@appraisalbuzz.com.

Share this article

Written by : Edward Pinto

Edward J. Pinto is a resident fellow and the director of the AEI Housing Center at the American Enterprise Institute (AEI). He is currently researching how to increase the entry-level housing supply for first-time buyers and renters who earn hourly wages, as well as examining the current house price boom that began in 2012. This continues his previous work on the role of federal housing policy in the 2008 mortgage and financial crisis.

Along with AEI Resident Scholar Stephen Oliner, Mr. Pinto created the Wealth Building Home Mortgage, a new approach to home finance designed to provide a more reliable and effective way of building wealth than is available under existing policies. This mortgage allows home buyers to maintain a buying power similar to a 30-year loan. It is aimed at a broad range of homebuyers, including low-income, minority, and first-time buyers.

Before joining AEI, Mr. Pinto was an executive vice president and chief credit officer for Fannie Mae until the late 1980s. Today, he is frequently interviewed on radio and television and often testifies before Congress. His writings have been published in trade publications and the popular press, including in the American Banker, The Hill, RealClearPolitics, and The Wall Street Journal. In addition, as the director of the AEI Housing Center, he oversees the monthly publication of the AEI Housing Market Indicators, which has replaced AEI’s monthly Housing Risk Watch and AEI’s FHA Watch.

Mr. Pinto has a JD from Indiana University Maurer School of Law and a BA from the University of Illinois at Urbana-Champaign.

Comments are closed.