The Collateral Risk Network, Inc. met last week in Sarasota, Florida to a packed house. We had a stellar line up of speakers including Brian Montgomery, the Assistant Secretary of Housing and Urban Development; and Lynn Fisher, the Senior Advisor for Economics with FHFA among others.

Liz Green of Loan Logics spoke on data in the modern age of appraisal. Liz has been actively involved in Mortgage Industry Standards Maintenance Organization (MISMO) for many years and is considered one of the leading experts. MISMO is responsible for developing standards for exchanging information and conducting business in the U.S. mortgage finance industry. Liz described the future of data as less a static form and more an expanding and collapsing set of data based on property type. There is a desire to shift away from free-form text in addendums to more discreet data collection that can be machine-read. This would not eliminate the comments in the report but help to distill the data down into meaningful and useful data. Ideally, providing a single presentation or view that presents a minimum standard set of data and then case-driven details. The appraisal process for residential property has always been affected by the role of the form templates published by the GSEs. The emphasis on data collection is paramount.

Lynn Fisher from FHFA stated that Director Calabria is focused on making FHFA a world class agency. Director Calabria has stated that Fannie Mae and Freddie Mac (“the Enterprises”) exist to ensure mortgage credit availability through the economic cycle. FHFA wants to ensure that each Enterprise operates in a safe and sound manner to ensure the health and welfare of the housing finance system. Lynn said, “We’d like to fix the roof while the sun is shining.” It is the goal of FHFA to foster a CLEAR National Housing Finance Market. CLEAR is an acronym for Competitive, Liquid, Efficient, and Resilient. The Director has asked Congress for additional authority to create additional agencies to increase competition. FHFA has asked the GSEs to hit the pause button on pilots. FHFA is currently doing outreach meetings with all the stakeholders to listen and get input on collateral risk. They are evaluating policy decisions.

It always makes for an interesting CRN meeting when a speaker reveals a little bit about themselves from the podium. Brian Montgomery is serious about the availability of affordable housing and delivers the facts with a quick wit, leaving the audience spellbound. With a memorandum from the President in September for Housing Finance Reform, FHA is working to expand access to qualified borrowers, implement Technological upgrades, and provide liquidity to the mortgage markets. Brian commented that he hopes to provide clear roles for FHA, Ginnie Mae, and the GSEs. FHA has increased the limit on the 203k program from $35,000 to $50,000. And, with the long-awaited condominium rule released in August of last year, it provides a vital source of affordable housing for first time home buyers and senior citizens.

Carol Trice, Zillow’s manager of home valuation analytics, walked us through the iBuying process. Carol shared a statistic where 95% of sellers said that at least one selling activity was stressful. This, among other factors, lead to Zillow’s creation of Zillow Offers. Consumers (home sellers) complete a questionnaire providing detailed information on the home including condition, quality, upgrades, known repairs, and other items which would influence the market price and salability. If the home qualifies, the seller would receive an initial offer to purchase from Zillow contingent upon an onsite inspection by a Zillow inspector. Internally, Carol’s department completes a valuation on the property which determines estimated days on market and number of days to market considering necessary repairs. Sellers are then given an updated offer on the property after the additional analysis. If the seller accepts the offer, they are allowed to choose a closing date up to 90 days out. Zillow’s business model is to make their money on the fees they charge for the service and not on the spread between their purchase price and the sale price. Zillow is not flipping properties in the typical manner but providing a service to the consumer which takes the stress of selling their home out of the equation.

Ed Pinto, Resident Fellow, and Shinai He, Research Analyst with the American Enterprise Institute (AEI), gave a preview of their most recent project detailing the value proposition of “walkability” to a property. Walkability is a measure of how friendly an area is for walking to amenities. Factors influencing walkability include the presence or absence of key conveniences like shopping, restaurants, drug stores, etc. Their research showed that consumers had higher appreciation in places with the highest walkability over properties with limited walkability. Ed is working to provide free data to appraisers who want to determine the walkability score of a particular property.

Trevor Taylor from the Open Geospatial Consortium (OGC) told us about their focus. OGC helps develop standards which cover a broad number of communities. From mapping inside a building which helps first responders know what they will encounter on any given call to their focus on underground infrastructure mapping.

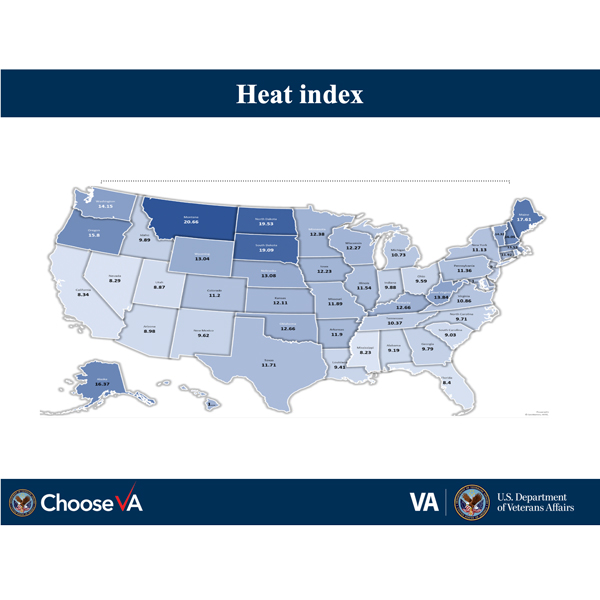

John Bell and James Heaslet of Veterans Affairs discussed the initiatives VA has implemented to increase customer service and reaction time to ensure veterans are getting the benefits they deserve in a timely and efficient manner. The VA is doing about 4,000 loans every business day. They have cut down the number of days it takes to determine eligibility from 23 days to just one on average. They implemented a new phone system which now gets veterans to a subject matter expert in record time. Not a recording or leaving a message, but a real person in the regional call center. Now that’s how you’d expect a veteran to be treated. The VA has about 6,700 appraisers and are still in need in certain markets. They have implemented the Assisted Appraisal Processing Program (AAPP) which allows appraisers to collaborate with one another. Appraiser Trainees are permitted to sign on the left. As a part of their modernization efforts, the VA now has VALERI, which provides an end to end look at the loan life cycle for veterans. It will help to make good underwriting decisions to better serve veterans. It makes one proud to know that the people in charge of the veteran benefits take such pride in improving the processes necessary to help veterans purchase their own home. The image below is a heat map of the average days from the time the order is accepted by an appraiser to the order being uploaded to the VA system.

The final presentation of the day was from the newly installed CRN Board of Directors. They elaborated on the new mission statement of the CRN:

Our mission is to instill confidence in the housing market by creating an environment that promotes safe and sound collateral risk practices, policies, and procedures under all economic conditions through education and collaboration. A vibrant housing finance system is at its best when it works for all stakeholders.

Our core values are transparency, integrity, and independence.

The CRN will work to expose, adopt, or promulgate standards necessary to ensure the safety and soundness of the housing finance system. The goal of the CRN is to bring together the different stakeholders through committee involvement. There are a number of committees with which the CRN will work to achieve this goal. There will be a focus on “How to Become an Appraiser” with a focus on virtual career coaching from volunteers within the CRN membership who can direct new entrants and answer questions on the process to becoming an appraiser. The leadership of the new CRN were clear in their focus. The CRN will not be an advocacy group for appraisers, AMCs, or any other sector of the industry, but will focus on collateral risk.

The new CRN website will be launched within a few weeks. If you are interested in learning more and becoming a member, please contact Karen Connolly at Karen@collateralrisk.org or 513-490-0226.

Have any comments or would you like to submit content of your own? Email comments@appraisalbuzz.com.

Share this article

Written by : Karen Connolly

Karen Connolly is the Vice President of Operations for Appraiser eLearning. Her responsibilities include overseeing the planning and execution of Valuation Expo, a prestigious real estate appraisal conference held annually in Las Vegas. In addition to her role at Valuation Expo, Karen provides valuable support to both Appraiser eLearning and Appraisal Buzz, contributing to their growth and strategic objectives. Karen has a bachelor's degree in Fine Arts from the University of Cincinnati.

Comments are closed.