Working through the new Market Conditions policy and advisory from Fannie Mae

Did Fannie Mae just throw a wrench into how residential appraisal reports for mortgage transactions are completed with their recent announcement on Market Conditions?

As an appraiser, it is highly likely at some point you will see the following or a similar request soon after your appraisal is submitted to your client, or even months after your appraisal is accepted by your client: Please provide support for your market conditions adjustment conclusions.

Appraisal Quality Control and Appraisal Quality Assurance create a revision request minefield filled with Lender and Investor tailored appraisal reporting requirements and preferences. Review of the appraisal reports is required by the lender or whoever the lender chooses to delegate this requirement to (i.e. Appraisal Desk, AMC, etc.).

Appraisal Risk Management processes, or Quality Control and Quality Assurance appraisal-related processes, are designed to:

- Identify current practices of both internal and external service providers

- Measure both actual and projected outcomes

- Create defined steps to ensure appropriate decision outcomes

Fannie Mae and Freddie Mac have recently aligned policy content when addressing the development and reporting of market value trends and the market conditions (or time) adjustments to comparable sales.

The latest advisory is a continuation of the trend to increase content to appraisers and lenders when Selling Guide Appraisal Requirements are revised.

As part of this recent advisory, the Fannie Mae guidance offers clarification of defining neighborhood and market area, and specifies that Market Trend conclusions and adjustment levels to comparables in certain circumstances may not be aligned. This is a concept not unfamiliar to the real estate appraisal professional.

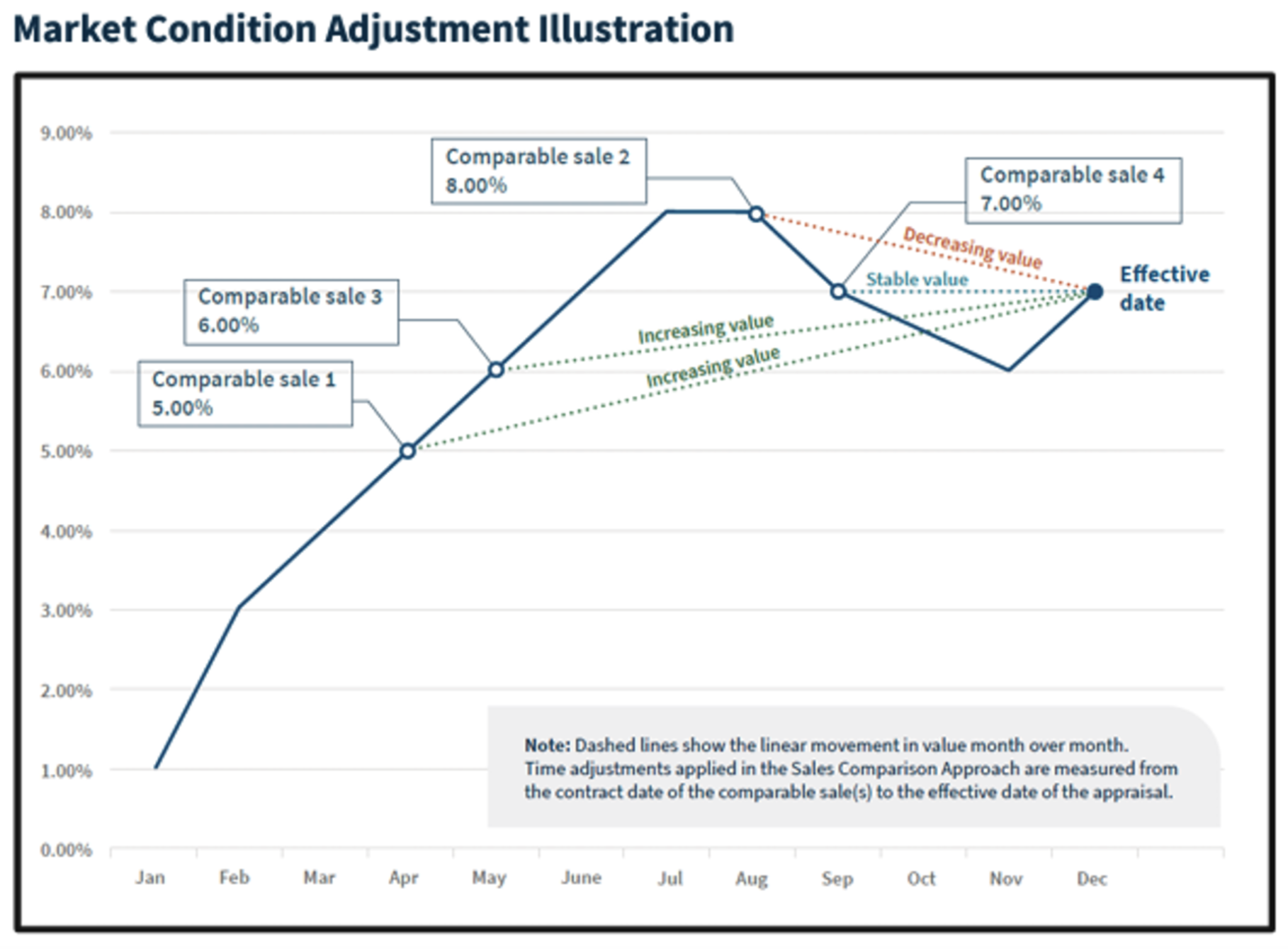

To illustrate how these two processes are embedded in the appraisal process, Fannie Mae has provided an example of a graph that captures a visual explanation of how the conclusions are applied for both the overall market trend (blue line) and the individual adjustment levels (callout data points) when applying adjustments in the Sales Comparison Approach.

As a practicing appraiser, the announcement and accompanying exhibit prompted a series of questions in my mind.

- Does Fannie Mae want to see this specific graph in all appraisals?

- What does USPAP say?

- What level of data and analysis does an appraiser need to present when providing support for market conditions adjustments?

The following is where I have arrived at developing answers:

#1. Short answer – No. Long answer: There is no expectation or requirement that every appraisal is to include a graphic identical, or even similar, to what was presented as an example in the FNMA advisory. This has been independently verified with the source. The graphic is a teaching tool that captures the trendlines of market value changes in this specific example, plotted over a 12-month period and calls out market change measurements between the comparable sales and the appraisal effective date.

While the chart provides a great visual of capturing these specific appraisal conclusions in the example, graphs showing these specific data elements and content may not be available to be produced for all appraisal assignments in all markets for a variety of reasons including availability of reliable data and availability of software tools.

To get to the specific guidance and policy requirements, the Selling Guide content has been updated as follows: “Time adjustments should be supported by other comparables (such as sales, contracts) whenever possible; however, in all instances the appraiser must provide an explanation for the time adjustment in the appraisal report.”

That’s the bottom line – explain the reasoning for the adjustment – don’t just state the conclusion(s). It is highly probable that the appraiser has developed the adjustments based on one of the acceptable methods of adjustment analysis (i.e. survey, statistical analysis, regression analysis, matched pair analysis etc.). The point of the Fannie Mae advisory is that the work can be shown through multiple formats, and may include graphs, charts or concisely and effectively worded summaries or a combination of all three.

#2: I am not a USPAP certified instructor and my expertise in USPAP is limited to my reading and attendance in CE offerings as an appraiser since its inception. I strongly recommend that appraisers, reviewers and any person(s) involved in the Quality Control/Quality Assurance process revisit USPAP Advisory Opinion 37 (AO-37), to refresh their understanding of both the requirements and expectations when managing the development of market trends conclusions and comparable sales adjustments.

#3: There are no prescriptive policy or advisory statements out there that give us step by step instructions on how much is enough to meet the standard. The measurement of compliance is that the appraiser completed analysis and reporting that is deemed acceptable by his/her professional peers. What is required is enough information to convey to the intended user, an acceptable level of confidence that market trend conclusions and any related adjustments are appropriately managed in the development of the opinion of value.

As both Fannie Mae and Freddie Mac have now gone on record on what their expectations are of both appraisers and lenders, it is up to each practicing appraiser to assess their current skill level, and when necessary, seek out refinements through education and other training opportunities to ensure success for their clients and for themselves. The more we build confidence in our services, the better the chances of sustaining our roles in the mortgage decision-making process.

Share this article

Written by : Ken Dicks

Ken is the current Director of Appraisal Compliance and Initiatives for Reggora, a leading appraisal platform. Ken has been a practicing Real Estate Appraiser since 1984 with a broad range of experience including independent fee appraiser, financial institution appraiser and reviewer, commercial and industrial Tax Assessor and manager of appraisal review