Unless you’re living under a rock, you have heard that interest rates have been rapidly increasing since Q1 of 2022. The average 30-year fixed rate mortgage rate was its lowest ever at 2.65% on December 31, 2021. It consistently climbed to 3.76% as of March 3, 2022, and as of the date I’m writing this, it is 5.81%.

Assuming a $250,000 loan was committed on December 31, 2021, your monthly payment was approximately $1,007 exclusive of escrow for real estate taxes and insurance. Fast-forward to today, and that same loan translates into a monthly payment of $1,468 – a 46% increase in monthly mortgage expense! Put another way, your $1,007 monthly payment based on a 2.65% interest rate will now translate into a $171,506 loan at 5.81% instead of $250,000 – an erosion of approximately $80,000 in buying power.

Naturally, this has forced buyers to seek lower price points or has completely eliminated them from the market. Therefore, it begs the question: what will happen to home values?

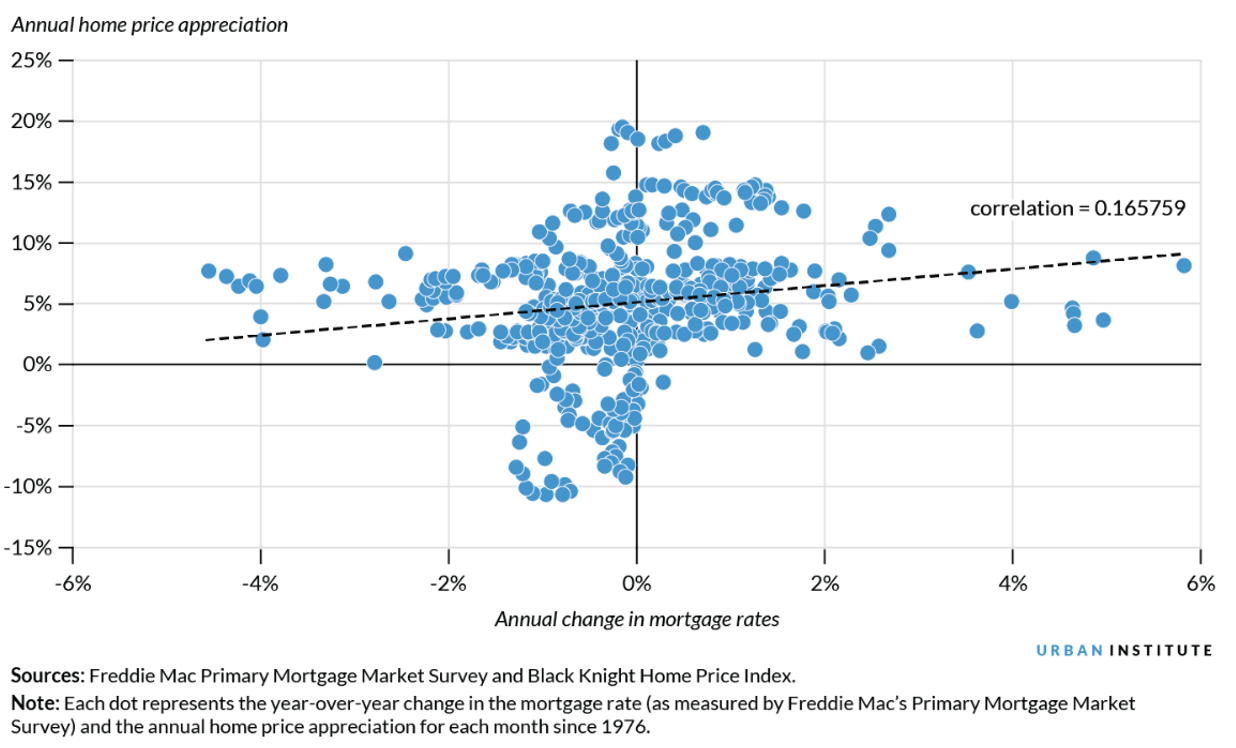

To answer this question, we must consider the historical correlation between interest rates and home price appreciation. Since 1976, mortgage interest rates and home price appreciation have had a positive, but weak relationship. That is, higher mortgage rates tend to occur alongside higher home price appreciation, but it is a weak tendency.[1]

The weak historical correlation suggests to me that – despite general consumer buying deteriorating with inflation and higher interest rates – these influences have less of an effect on the upper-middle to upper-class market participants who remain in the market, primarily as investors. These demographics were the participants winning deals before interest rates rose (with cash) and will remain the ones winning deals now and into the future. This is a trend that leads me – and many others – to believe that we are quickly transitioning into a renter economy – much like the United Kingdom where their homeowner has fallen from 71% in 2003 to 63% in 2018.[2] This trend is almost certain to increase the wealth gap between rich and poor in our country and may provoke steep measures such as federal rent control in the future.

The “weak” correlation between interest rates and home values may also be attributable to the balance of supply and demand. It has been advertised that most markets lack substantial supply of homes – especially for low- and moderate-income housing. This imbalance is another contributor influencing home values despite rising interest rates and is a consideration to be aware of when analyzing the current market.

Another trend to be aware of is the days on market metric. Days on market (DOM) for residential property in most markets throughout the country are increasing; however, DOM is still historically low in most of these same places. This trend is really a reflection of the market normalizing/stabilizing than decreasing.

Increasing DOM is not necessarily correlated with decreasing prices, but it does mean buyers will have more choices and will be able to regain some bargaining power in negotiations. This might manifest itself with lower offers that are acceptable to the seller, but price isn’t the only aspect of a transaction. Terms of a transaction is typically where you’ll find buyers tipping the scale back to even in negotiations before there’s an influence on price. This transfer of negotiating power has already begun with many buyers now being able to elect contingencies such as inspection and/or appraisal – each of which was difficult to include in a competitive offer as recently as 1-2 months ago.

Based on the preceding discussion, I’d contend that prices are not actually as susceptible to decreasing as many think. I believe buyers may actually be able to take advantage of the perception of a volatile market right now. Anecdotally, sellers are worried that the threat of increasing interest rates with continue to erode buying power which will have a negative effect on their sale price now and especially in the future. Sellers are panicking right now which is almost always an opportunity for buyers. It follows then that this might be the best time to get a deal – residential or commercial.

Take a recent example of mine. I was in the market for another single-family rental investment in Lancaster City. I was in the market for about a month and placed an offer of $270,000 on a $285,000 listing. I waived no contingencies. This property had only been on the market for five days. The offer was accepted.

Average days on market in Lancaster City in May 2022 was 13 compared with an average of 25 DOM during the last 24 months. Home prices have increased during the same period by 69%.[3] This is qualified as a rapidly increasing market.

Now, let’s compare recent trends to historical trends. Over the past 10 years, Lancaster City homes were on the market approximately 50 days before being placed under agreement. Therefore, if we can agree that we are no longer rapidly increasing, but stabilizing market, it follows that DOM should trend closer to 50 for current listings.

Based on the above, it follows that the sellers in my scenario are doing themselves a disservice by not leaving their home on the market for a longer period of time. I would qualify the sellers acceptance in my example as irrational and atypical given a stabilizing market. This type of counsel must come from a REALTOR who can explain the exact scenario described above.

So, how do you comp in this market? I think you use recent sales and make no adjustment for a decreasing market because I’m not convinced that’s what’s happening. Sellers are accustomed to less than 2 weeks on the market which is simply not typical. This preconceived notion may be derived from national news or friends outside of their market area – but remember, real estate is specific to submarket and these anecdotes are rarely, if ever, universal.

In Lancaster City, for example, we must be weary that any sale going under agreement in less than 2 weeks in the current market is reflective of “market value.” Market value may actually exceed the sale price in most instances if you can support that the seller is acting imprudently – and inconsistent with the definition of market value. These concepts are what appraisers refer to as the relationship between “exposure time” and “conditions of sale.” This relationship is incredibly difficult to credibly defend; nevertheless, it’s important to be critical of these situations because there may be external factors influencing the data. Simply put, there’s a difference between 1) sale price with conditions of sale, and 2) market value – which is based on typical buyer, typical seller, and adequate exposure time, among other criteria.

[1] https://www.urban.org/urban-wire/how-higher-mortgage-rates-have-historically-affected-home-prices

[2] https://www.brookings.edu/essay/uk-rental-housing-markets/

[3] https://stats.brightmls.com/listingAnalytics/ms-report

Share this article

Written by : Mike Rohm

Michael J. Rohm, MAI, CCIM, R/W-AC, is an appraiser and sales agent working throughout Pennsylvania. He is Owner and President of Commonwealth Commercial Appraisal Group and is Director of Valuation Advisory and Senior Associate with Landmark Commercial Realty.

3 Comments

Comments are closed.

Some very good points especially the growing gap between the haves and have nots. Homes in the grand rapids area sell in less than 5 days with overbidding still. why? there are buyers who if needed can put down an extra 15,000 to keep their payment reasonable. have some been entirely kicked out of the market? I know a number of people. as for trying to find a rental? Nearly impossible in my area with rents above 1200/mo for 1-2 bedrooms. what does a family with 2-3 kids do? there is a crisis here that needs further delving into. as for values declining. no way. the bar has been set.

[…] Today’s Buzzcast interview is with Mike Rohm of Commonwealth Commercial Appraisal Group. We sat down with Mike and Joan Trice, Founder of Allterra Group, LLC, to discuss his latest article in Appraisal Buzz, “Market Correction or Seller Panic?” […]

[…] Today’s Buzzcast interview is with Mike Rohm of Commonwealth Commercial Appraisal Group. We sat down with Mike and Joan Trice, Founder of Allterra Group, LLC, to discuss his latest article in Appraisal Buzz, “Market Correction or Seller Panic?” […]