It’s been called an “appraisal time bomb” by some, while others say it’s no biggie. Today I want to give you the scoop on what it is as well as some of the potential impact it might have.

What is Collateral Underwriter?

Collateral Underwriter (CU) is a property appraisal review tool created by Fannie Mae to help mortgage lenders manage risk.

What will Collateral Underwriter do?

- CU performs an automated risk assessment on appraisals geared toward Fannie Mae and returns a risk score, flags, and messages to the submitting lender. CU will provide a risk score for the appraisal of 1-5 (1 being the lowest risk and 5 being the highest).

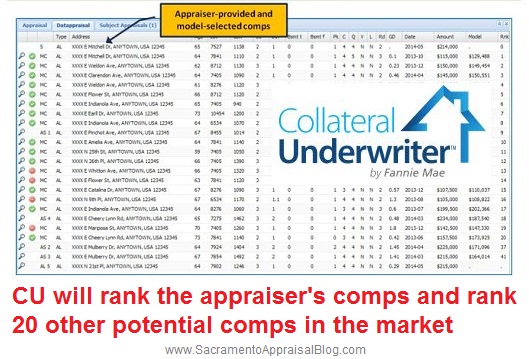

- CU will analyze comparable sales selected by the appraiser and recommend alternatives.

- CU will compare adjustments the appraiser has given with what other appraisers have done in the same area (Fannie Mae has been mining data from over 12 million appraisals since 2011, so they definitely have some data at their disposal).

- CU will use census block groups to analyze market trends.

- CU will review specific information in each appraisal such as the sales price, lot size, bathroom count, bedroom count, age, location, size of the basement, condition, quality of construction, view, and GLA (gross living area). In 2011 Fannie Mae mandated appraisers to begin using UAD codes in their reports to describe all of these elements. You may have read a report and thought, “Why the heck is the appraiser saying the property is in ‘C4′ condition? What does that even mean?” Well, that is a Fannie Mae UAD code to describe a specific condition, and now that Fannie Maw has over 12 million appraisals in their system with these codes, it has allowed Fannie Mae to give birth to the CU review tool.

5 things to know about Fannie Mae’s Collateral Underwriter:

- Fannie loans only: CU is only used for loans geared toward Fannie Mae, and not for divorce appraisals or any other private appraisals. CU is also not used on 2-4 unit properties or “drive-by” appraisals.

- Not FHA/VA: CU is not used for FHA and VA loans (I’d be shocked if they didn’t adopt it later though).

- Commentary: The CU tool does not read any of the commentary by the appraiser, which can be key to understanding comp selection, adjustments, and the final value.

- Neighborhood boundaries: CU uses census block groups for data analysis instead of specific neighborhood boundaries that may be readily understood in the market. Pulling data from the right neighborhood can make a HUGE difference in a valuation, don’t you think?

- Adjustments & comps: Fannie Mae has heaps of data to compare to any new appraisals that come into the system. Not only do they know about sales in the neighborhood, but they also know which comps other appraisers have used, and even value adjustments given by other appraisers. CU knows if an appraiser says a comp is in good condition (C3) in one report, but then says it is in fair condition (C5) in a different report. CU will pay special attention to comp selection, adjustments, and the final reconciliation of value.

Potential Impact of Fannie Mae’s Collateral Underwriter:

- Unknown: The truth is we don’t really know how CU will impact the market. It could be a game-changer for the mortgage industry and appraisal profession, or it could feel like the same old same old.

- Slower loan process: As CU is implemented, expect a learning curve, and thereby a slower loan processing time. It’s going to take some time for lenders, appraisers, and underwriters to work out the bugs.

- More conservative appraisals: One of the unintended consequences of CU may be more conservative appraisals.

- Headaches for appraisers: The fear among appraisers is that lender clients will now come back to say, “CU has identified 20 other comps in this census block. Why did the you not use these?” Hopefully that will not happen (assuming the appraiser did a good job of course), but increased scrutiny will be bound to cause appraisers to spend more time responding to CU.

- Higher cost for consumers: If CU does end up putting more work on appraisers, it may lead to higher appraisal fees. After all, more work requires more time (which is money).

Advice to the Real Estate Community:

- Real Estate Agents: Make sure your clients know how strict the underwriting process has become for appraisals. I’m not saying you need to sit down with your clients and watch Fannie Mae’s CU tutorial (that’s probably a quick way to lose clients). All I’m saying is this is one more reason to price properties correctly since the appraisal is going to be even more scrutinized now. Also, if you accept an offer that is clearly out sync with neighborhood values, the lender is going to have a ton of data at their disposal about neighborhood values – even if the appraiser happens to “hit the number” somehow.

- Appraisers: Many appraisers are gravely concerned about CU, though many lenders have been reaching out to say, “Hey, we’ve already been scrutinizing you, so don’t worry about this.” Only time will tell how this will impact business and the industry. All we can do is choose the best available comparables and make reasonable market-supported adjustments. There will be a learning curve to know how to avoid red flags so to speak, but explaining why we made adjustments and supporting those adjustments will be a big theme this year for lender work. The bottom line is appraisers will need to add more commentary in their reports. If you are making the same adjustments in every single report regardless of the location of the property, it’s time to stop that because adjustments vary depending on the neighborhood. If you are struggling to support adjustments, it may be a good year to find a mentor as well as take some quality continuing education. If you do not know how to graph sales, make that a top goal this year. On the other hand, if you are an experienced appraiser, find ways to be a mentor to other appraisers by answering their questions – whether on forums or in person. As I said in 10 things appraisers can do to improve the appraisal industry, “Too many appraisers think they are right about everything, but at the end of the day being right doesn’t help anyone grow. Find ways to share your knowledge and build others up.” Lastly, if it ends up costing you more time to do your work, it may be time to consider raising your rates.

Reprinted with permission from Mr. ’s blog at sacramentoappraisalblog.com.

Share this article

Written by : Ryan Lundquist

Ryan Lundquist is a certified residential appraiser in the Sacramento area. Ryan runs the Sacramento Appraisal Blog, which is a top-ranking appraisal blog in the United States. He has been quoted in local and national publications and has been involved with the Sacramento Association of Realtors for nearly a decade. Ryan is also a board member of the Real Estate Appraisers Association of Sacramento. His clients include home owners, real estate agents, governmental agencies, attorneys, and lenders. Ryan also won the Affiliate of the Year award in 2014 from the Sacramento Association of Realtors.

47 Comments

Comments are closed.

Meanwhile, the Fannie Mae idiots are doing 3% down deals. So what happens? Seller wants $300,000. Buyer needs $9,000. Instead, sale price becomes $310,000 and the buyer gets $10,000 cash back as a seller concession. Voila! 100% financing. But are they worried about this? No, they are worried about whether you called something C3 and somebody else called it C4. Or why you didn’t use a certain sale in your census tract, when no appraiser on the planet ever appraised using census tracts. IDIOTS!!!!

That’s a new one I never heard of before. Census Tract, are the sales within 1 mile of the subject? And don’t forget to raise your fees, with all the call backs that will be coming you will deserve it.

And so it starts…. Here is a revision request form a national lender I received today. How would you respond?

****UNDERWRITER REVISIONS****

Message – Comparable 3 (Collateral Underwriter)

The condition rating for comparable #3 is materially different than what has

been reported by other appraisers. Please provide supporting commentary for

your data on this condition.

Message – Comparable 3 (Collateral Underwriter)

The quality rating for comparable #3 is materially different than what has been

reported by ot her appraisers. Please provide supporting commentary for your

data on this condition.

Message – Comparable 2 (Collateral Underwriter)

The quality rating for comparable #2 is materially different than what has been

reported by other appraisers. Please provide supporting commentary for your

data on this condition.

Yeah, so I saw a lot of print about how it would adversely affect the chop shop appraiser who doesn’t do their due diligence. My day one experience with CU was about my gla for comp 3 being larger than public records and that reported by my peers. Well, public records has comp 3 as a 1274 sf cape cod, which it was in 2007 at its prior transfer. But now it’s a colonial and apparently my peers just simply copied public records without actually looking at the house. Perhaps there are more appraisers NOT doing their due diligence and CU will mean more stips for those of us who look at the data critically. After all, CU is a computer program and as long as you do what the herd is doing, it won’t notice you.

Wow @disqus_19t6sd5ZJw:disqus. How can a supporting commentary be given without more specific information from other appraisers?

Ryan, this is the verbatim message copied by the underwriter from CU and pasted in to a revision request. There was no thought or triage by the underwriter. They did not read the report or comments which address this issue. They are basically forwarding the CU message. A trained monkey could to it.

It does sound like a forward to me. More time = more money. Should be interesting to watch how this all unfolds.

I would ask for more money every time they come back just for a question. You know the AMC crackers get atleast 450 for there appraisal they give appraiser 250 for so they have the money for your time. Just ask, they will say its part of the scope but tell them you wont answer till you get a fee increase and the needed docs to accurately respond to there questions, LOOK A LAYWER WOULD NOT WORK FOR FREE SO WHY DO APPRAISERS. EVEN If you call a lawyer they still charge you for a phone call

Well, that is easy

Dear Lender,

please provide the data that shows this materially

different to in fact be the true.

I can not comment on other appraisers work or data without first reviewing that data.

I wait for your reply

Thank you,

GLA, site area, room count and number of garages is fair game, as is consistency by the individual appraiser (call a comp C3, it’s always C3). But no to quality and no to condition. Those are subjective calls.

Good post Ryan, keep up the good work

Thanks Brian.

Collateral Underwriter should be renamed “COLLATERAL GOTCHA”.

I believe the most likely future scenario:

Residential Appraiser’s;

Will low-ball their value opinions (deal killers) and minimize all adjustments to avoid excessive CU “gotcha” scrutiny

Will decline all orders in non-cookie cutter neighborhoods that don’t have a massive number of “approved” Comps.

Will let appraisal orders and/or stip requests languish on their desks indefinately because they don’t want to justify an adjustment to an underwriter in another city who is following the review template, which will allow loan locks or contract dates to fall through.

Will raise appraisal fees to a much higher rate to account for all the extra time spent on time consuming report writing & nonsense stips. No longer the nice “flat rate fee” amount the homeowner & lender could depend on.

This over reach is much more than just some minor tweak that will only affect the appraisal profession. It has the potential to screw up the entire real estate market in all areas. CU will not be good for anybody, Appraisers, Realtors, Lenders, Builders, and of course, the most important segment, the Home Buying Public.

I appreciate your take, and I love your slogan “Collateral Gotcha”. :)

Thanks Ryan.

We’ll see, but I have a feeling this latest CU over reach may eventually become known as “Appraisergeddon”.

By the way, I used your “Collateral Gotcha” line in a presentation to agents this morning on CU. It got some good laughs. I attributed it to you and didn’t take credit.

Thanks for the acknowledgement. But, I bet those agents won’t be laughing in a few months when their deals crash because the appraisal they needed to get their deal closed has stalled in traffic ( e.g. underwriter stips that go unanswered).

That could happen. Some deals simply won’t work though no matter what because of quality issues – CU or not. I’m not saying CU is going to make it easier though.

Ryan, of course, only time will tell….and I’m not ordinarily a doom & gloom guy. However, CU’s message to appraisers is basically “we don’t trust you”, and this is likely the third strike to the appraisal profession, at least as we now know it (Dodd-Frank, AMC’s, & now CU).

I’ve been a State Certified Appraiser since 1996, and experienced a lot of ups & downs. But, I predict it won’t be much longer before far too many good appraisers will get fed up with an inordinate number of CU nit-picky stips that didn’t exist before now.

I think CU frustration will cause many appraisers to either refuse Fannie/Freddie lender’s orders (like me), expect payment in advance, drop clients, raise their fees significantly, or drop out themselves altogether. My 2 Cents.

Agreed on some appraisers leaving. The industry has changed dramatically and there are many uphill battles for appraisers. Yet to play devil’s advocate, many appraisers are working for bottom feeder clients and they simply need to get better clients.

appraisers should walk and stick together for more money from the greedy AMCS. This is not going to get any better for anyone. Appraisers are wimps and work for chump change and get bossed around by the MAN. MAN up appraisers and take your profession if you want to call it back BACK.. This is a joke… Appraisers working for under 250 on appraisals.. Why would anyone do that…. MAN UP and SHOUT until you get your fee

WOW it said this “The bottom line is appraisers will need to add more

commentary in their reports” but also said The CU tool does not read

any of the commentary by the appraiser, which

can be key to understanding comp selection, adjustments, and the final

value.

So we have to add a ton of work into the report that will not even get read, NICE

James, this commentary is something simple from the appraisers side that will become easier over time, the lenders position has changed with CU and is much different then from it has been in the past. I don’t think appraisers fully understand the implications of what CU means to a lender. What is essentially happening is that lender is “Certifying” they checked everything out and that the appraisers information is fully is accurate and that even though FNMA has found some differences with the appraisal the lender is saying “We know this and we accept this”. When it comes from a liability standpoint the appraisers are for the most part off the hook as the lender is now saying “We checked everything out”. From the standpoint of getting sued or having multiple revisions on a file I think those days are numbered as FNMA now or any investor is going to go back to the lender and say “You certified that this was right, you’re responsible for this”. The appraiser didn’t have access to the database and as a result is protected by USPAP. CU is going to change appraisers liability and repurchase risk big time. I think that this commentary is the short term is going to be something that benefits the appraiser in the longterm.

I don’t see that, I have had my first one come back already. The lender (AMC) wanted every detail as to why my data was as I reported and why it did not match public records. I had already made two full pages of comments on this one as nothing matched, but as was pointed out, no one read those. Play map shows 270×150 (40,500 sq ft) but public records show 45,080. Clearly the public records are incorrect. I included the map and wrote 6 lines about it in the addendum. Still was told by the lender I was WRONG and needed to fix it or explain why I was right. Even after I pointed out it was already in the report and made the AMC look at the map they still wanted me to change it to match public records. I said NO

3 days of this type of crap when on until I looked up the lender on the internet and got their phone number on the 26th. I emailed the AMC (Clear Capital) and said that if they failed to send the report to the lender that day I would call the lender and that I would send the report to them myself. I included the lenders phone number in this email.

BANG, within 30 minutes I go an email from the AMC telling me that the report had been sent to the lender and that my invoice was sent to accounting to be paid

Note, I raised my fees $50 this morning and now also include in processing fees on top of that. Last year my 1004 average fee was $417 and I expect it to go much higher before this year ends

All good feedback, I agree fee’s should be raised very quickly. I’m going to e-mail a few of my press contacts, would you mind being in a story about this?

Again, these are direct cut and paste from CU by the underwriter and passed to the amc clerk and forwarded to the the field appraiser. No qualified review appraiser screened these for ‘false positive’:

Reason for Revision

Message – Appraisal (Collateral Underwriter)

The appraiser-provided comparables are materially different than the model-selected comparables.

Message – Comparable 4 (Collateral Underwriter)

The GLA adjustment for comparable #4 is smaller than peer and model adjustments.

They provided me with 14 suggested comps, five of which I utilized in the report and 3 which are located in a different town.

Well, here we go…just got our first urgent request to address CU issues. This is gonna’ be fun. This should drive the last good people out of the industry. Here’s a few samples: 1) The condition rating for comparable #3 is materially different than what has been reported by other appraisers. 2) The GLA adjustment for comparable #1 is smaller than peer and model adjustments. 3) The lot size adjustment for comparable #3 is materially different from peer and model adjustments. 4) The quality adjustment for comparable #1 is smaller than peer and model adjustments.

my biggest issue is this one

I inspect a property for a sale. I walk through it, around it, look under it and in the scuttle. I see many things that no one else sees. I write a report and call it C4.

After it sells 6 other appraisers use it as a comparable. They have not seen it up close. All they see is what the Agent puts in the MLS and what they can see from the street. The Agent is NOT an unbiased source of data and calls out every thing as great and wonderful. The other appraisers all rate the house as C3, but none have truly seen the house.

CU flags me as being out of line with other appraisers in my area and I get a letter and maybe put on the watch list.

If the facts be known, it is the other 6 appraisers that should get a letter.

To take it one step more, it is the Agent that should have his/her license reviewed for NOT reporting the true condition of the subject in the first place.

HOW DO WE FIX THIS

Easy, we get the MLS (or force it) to provide data fields on the MLS that ONLY appraisers can put data in. ONLY the appraiser that does the inspection and report for the property. He updates the MLS with Q and C ratings, Taped off Sq Ft and has an area to add in any notes from the inspection

This area can ONLY be seen by other appraisers as part of a new custom printout and should then be part of the work file.

Not rocket science, just a simple fix for the system

But until Fannie Mae can put a thumb on the Agents that junky house will always be reports as a creampuff

Great idea but my primary mls doesn’t even provide the data for the MC form. Letting an appraiser add to an MLS entry might cause someone a stroke.

I have one MLS that no longer reports seller’s concessions. There isn’t even an area on the printout. When I called the MLS customer service rep to ask, they said it’s really not necessary. Are you kidding me ? I have to email every realtor. Most don’t even bother to answer. Real nice

CU will go away if appraisers stand up to it! When you get a explanation/clarification requirement DEMAND to see the data. Your due diligence, is your due diligence. What

others rated a comp may be totally erroneous. You may have personally inspected the property. Six other appraisers are working from MLS data that was supplied by incompetent real estate agents.

Mike, part of me wonders if CU will flag appraisers when they don’t use the GLA from Tax Records. For instance, if Tax Records says 1274, but I measured 1283. Would it flag me?

I hope not but see James Falcon Pratt’s comment below. With all of the UAD appraisals Fannie has … it would be interesting to see the differences between the data of the appraiser who does the inspection compared to the data available through public records and the appraisers who use the property as a comp.

ok, Just redid my fee schedule after having a talk with 5 other appraisers in the county. we were all over the board on how much to raise them and what to charge for additional comparable research. I was already one of the higher fee guys so I only kicked my minimum fees $25, other $50 and one guy $75.

Additional research costs from appraiser to appraiser were talked about if it depended on driving to the properties or just researching the MLS and calling agents. These fees took on a life of their own, ranging from $15 to $50 a property.

I understood the $50 (seemed a bit high in my eye) if you were required to drive back up into the mountains on dirt road to take a photo. But I had no issues with $15 per property and using the MLS photos to show I researched the property. I even said I would include the MLS Listing sheet in my report. I can see adding up to 20 of them and making my now 35 page report become 55 pages.

One guy said he wanted to require the Lender/AMC to pay for this research COD. He would get the list and send them an invoice with a letter explaining than he would be happy to research the additional properties AFTER they had paid the fee for such work.

In the end I see this will bring us together or end the use of appraisers. We will stand up and say NO or will will be picked off one by one until very few remain

The problem is this: Fannie Mae has publicly stated

that most comparables have been rated for condition and quality by five or six

other appraisers. What CU is really saying is that the majority of appraisers

have ‘outvoted’ you. It’s an uphill battle to prove the majority is wrong, and

if you don’t defend yourself then you risk being flagged for 100% review which

is tantamount to a foot in the Fannie Mae graveyard. Even if you do defend

yourself you still may be flagged if you get outvoted too often and are

considered ‘high risk’. Remember, CU does NOT read comments and it appears that

underwriters and amc clerks are not proactive in triaging these flags. No

matter how well an appraiser documents their ratings they will still get these

automated flags. Who is going to pay for the extra time it takes to

meticulously defend appraisal reports?

The “Summary” comments about CU are just another Fannie Mae jab at appraiser’s who are victims of Form Reports. They want Narrative Reports (without paying for them) on a Form that is Summary in nature. The biggest issue I am afraid is “The Black List”. If I have read correctly the Appraiser’s are the ONLY people who cannot see this list. If we are being held to this witch hunt why are we the only ones that cannot access this list? We are licensed professionals who from state licensing boards to Fannie Mae are always “Guilty until proven innocent”. Am I the only one who thinks this isn’t right?

Hello Mike

I can email you a speadsheet that will take the data and fill out the 1004MC, One-Unit Housing area and provide you with the Median DOM for your report.

All you need is an output file that has List Price, Sold Price, List Date, Contract Date and Closed Date and Status (Closed-Pending-Active). Most if not all MLS systems will give you that data. It also gives DOM in Max, Min and Median so you can comment on that. There are also a large number of charts build into the spreadsheet that you can copy/paste right into a picture window or text addendum in your report.

It also gives data on REo and SS properties if you used them in your 1004MC data block

I will be happy to email it to any one and can always be emailed or Skyped with questions should you need to ask

email – james@prattsappraisals.biz

Skype – falcon1229

With more questions being asked every day it is good to have this data at your fingert tips.

Demand to talk to chief appraiser at the AMCs. They hide behind the clerks

that work for them. If enough appraisers would refuse to talk to the clerks

then these issues will get resolved. AMCs are staffed with college kids that can’t

find jobs. They are working off checklists. You have a right under USPAP to talk to the chief appraiser!

When I get a request for additional information from an AMC (which is usually already addressed in the report), my immediate reply is: “Please provide the name, license number and state where licensed of the certified review appraiser requesting this information.” If the reviewer is not qualified to appraise the property, s/he is not qualified to review my report.

Here is a generalized reply I am crafting. Your input is welcome:

It appears that the lender’s staff (underwriter) has opted

to bypass Fannie Mae’s proscribed guidelines of routing these CU flags to the

appropriate qualified staff appraiser for review before passing them along to

the lender’s designated appraisal management company. The AMC has also opted to pass along these CU flags without a review process by a qualified staff appraiser. Had either party followed Fannie Mae’s publicly published process the qualified review appraiser would have had the opportunity to read the comments in the existing report which addresses the issues raised by these CU flags. Thank you for the opportunity to bring clarity to this issue and to point out that the existing comments in this report adequately address these CU flags.

Collateral Undertaker is living up to it’s name in spades. 125 comments (complaints) on TheNationalRealEstatePost with regard to their top two CU articles. If you’re willing to write a weekly reality series named “Last Appraiser Standing”, NBC is willing to offer you a contract. Someone may as well make a mint off of FNMA latest dumb ask move.

I would be happy to do the “Last Appraiser Standing” if I don’t have to use my real name. Fannie Mae would read it two or three times and Black List me for sure

I just turned down an FHA report for a property in the county that a year ago I would have done without question, for $650. I was the 6th appraiser that the AMC called and I am from the next county. Thanks to the CU system this will never fly due to GLA, Site Size and age. Between the those three items ther will not be a single comparable that will have gross adjustments under 25%. GLA is not a common public record in that county and the public records almost never get updated if there is an addition at any time. Most outbuildings like shops, barns and the like are built without permits or records of any type.

The result of properties like this in the county (outside of the city limits) is that no appraiser is willing to take on Fannie Mae and/or FHA for the $650 offered. The risk is just too high.

We now have five certified appraisers in my county that will not do any thing outside the city limits. Three have said they will hold that line for no less than the first year of CU to see how it plays out.

Maybe I’m missing something in the fine print.

Is CU only a reviewer tool?

Why isn’t the CU database available to appraiser use?

I find (and I know it takes more GD time!) comment comment on the sq foot differences. I put my important comments in CAPS or Bold text. From what heard the past 10 days from UW’ers, many of these silly stips just require us to comment. Then the UW can override the CU stip and clear the report. However our opinion of C or Q ratings are just that. Not sure how we reply to that. “IMO, I consider comp #__ a C3”. I don’t know for fact, but I can’t imagine the stips like Mike got will hurt his score card in the eyes of fannie.

ok, just came across another issue when I was doing an inspection just a few houses away from another appraiser doing one too

The house he was working on was for a Refi, the owner had purchased it just a year ago and the owner gave him a copy of the original report.

The house is clearly a C4 and the owner said he has not done any thing to it from the time of the purchase. The original report, done by a different appraiser, shows the property to be a C3, but it cleanly was not.

What is the new appraiser to do?

If he tells the truth and calls it a C4 he could get flagged for not matching the data that Fannie Mae already has on the property, so that is out

So

He is going to LIE and say the property is a C3 so no flags get tossed on the play.

The problem with the system is the once the first report is completed and sets a data base in Fannie Mae’s system, the original appraiser has set the standard and any one that come by later and does it correctly will be flagged. When what should happen is after the property collects 5 or 6 data points the original appraiser would be found to be out of line and that appraiser should be flagged.

This is going to create more and more lies in the system

Ok, issues within the Appraisal World

1 – We need new forms that are designed by Appraisers

2 – DO NOT provide a Sale Contract to the Appraiser, just provide an address and contact for access. Sales Contracts will always provide a Value for the Appraiser to to with that should not be there

3 – Get rid of the C and Q pegs. No house other than a New Construction fits into these concrete holes

4 – STOP the AMCs from telling Appraisers they MUST USE pre-printed statements provided by the AMC in the report. If they want their words in the report MAKE THEN SIGN IT too.

5 – STOP the use of OUT OF STATE or even OUT OF THE AREA Appraisers to review reports. You can not tell me that some one from Chicago, Boston, New York or Miami has any idea what the subject neighborhood makeup is in the rural parts of Northern California.

BIGGEST THING ABOUT LENDING

No Property goes into Foreclosure due to a BAD Appraisal

The report, house, property, appraiser, lender, underwriter or agents are not the reason for a load going bad.

THE ONLY REASON is that the BORROWER fails to make the payments.

No report, no mater how good or bad, can make the borrower make the payments

WRONG, WRONG, WRONG. Why would an owner want to pay for something you appraised for 50% below of what they were told 5 years ago was appraised $100K higher? You guys (appraisers) are allowing Fannie, Freddie, Frank and Dodd to ruin the real estate market. YOU!!!! Owners are walking away from what they took years to be able to purchase. Houses are becoming similar to cars. You value a home and then as soon as you move in, boom, worthless because CU says so. Grow some and point the finger where the issue is….United States Government….Uncle Sam.