This article is featured in the 2025 edition of the Appraisal Buzz Magazine. Some other features in our magazine include funny Buzztoon comics, industry trends, as well as crazy stories from appraisers and readers like you! Read all these articles and more in the latest edition HERE. If you want to make sure you are receiving the print version of the Appraisal Buzz magazine in your mailbox, sign up HERE.

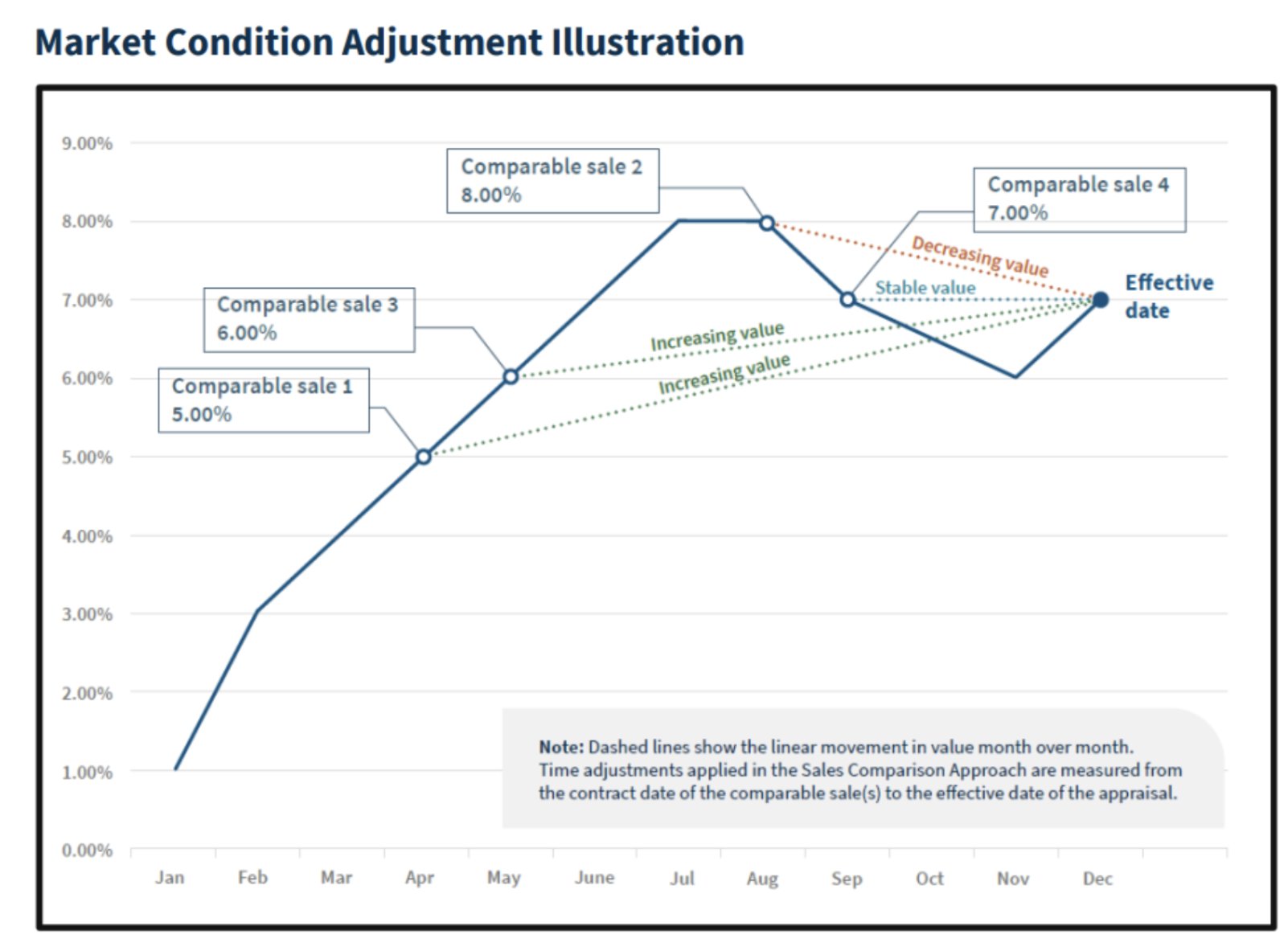

For decades, real estate professionals relied on established methodologies to evaluate market trends and develop market-to-market adjustments. However, on November 6, 2024, while I was teaching a CE-approved class on the topic, a seismic shift occurred. Fannie Mae released an example of how appraisers should be adjusting for market change.

An Old School Method: Grouped Data Analysis

I was teaching a method that relied on grouped data analysis, a method rooted in statistical rigor and detailed in The Appraisal of Real Estate, 15th edition. Grouped data analysis involves organizing sales by an independent variable, such as the date of sale, and comparing average prices across time periods. Specifically, this technique examines the average price of at least 30 sales over the most recent 365-day period compared to the prior 365-day period. The requirement for a minimum of 30 sales stems from the Central Limit Theorem, as explained by Marvin Wolverton, PhD, MAI, in An Introduction to Statistics for Appraisers. Wolverton emphasizes:

“Therefore, n >= 30 criterion generally applies to real property valuation work.”

By ensuring a sufficient number of observations, appraisers could derive reliable rates of change, spreading adjustments like a 3 percent annual rate across the year. While statistically sound, this method assumed that market behavior was consistent over time: a premise that does not align with the realities of seasonal markets.

The Tipping Point: Fannie Mae’s Requirement

Fannie Mae recognized the limitations of annualized rates; the new requirement emphasized the importance of accounting for intra-year market variations. This shift acknowledged that market change is not always linear.

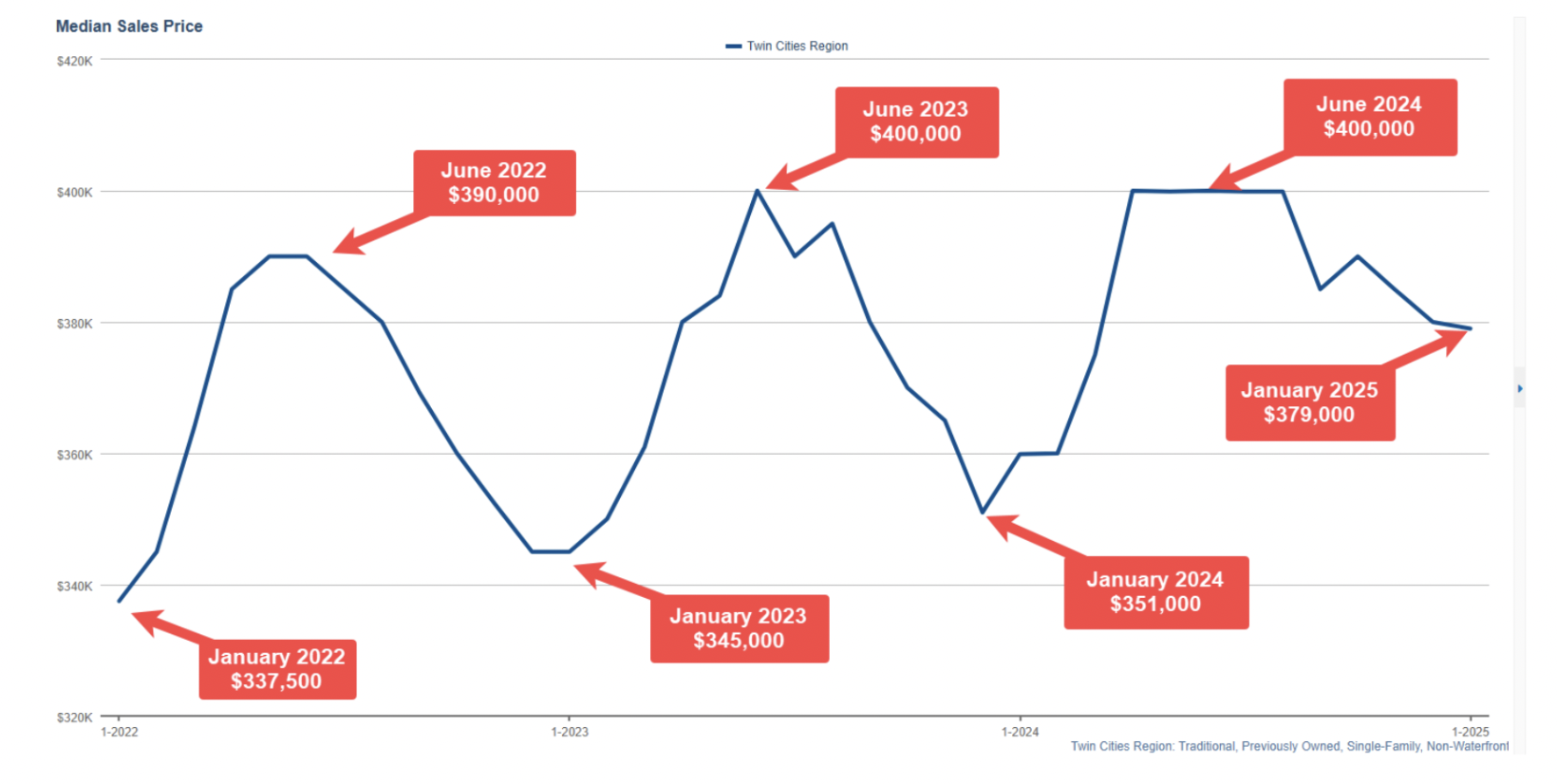

Take the Minneapolis/St. Paul region, for example. In this highly seasonal market, prices fall during the coldest part of the year and peak in the summer. Year-over-year changes, such as a modest $10,000 increase from June 2022 to June 2023, failed to capture the $45,000 drop from June 2022 to January 2023, followed by the $55,000 run-up to June 2023. This chart from InfoSparks shows the cycle repeating itself like a sine wave year after year. Other factors are in play, such as affordability driven by interest rates, but the fluctuations are clearly seasonal. Annual rates of change, spread evenly through the year, are not the answer.

A New Way Forward: Trendlines and Seasonal Adjustments

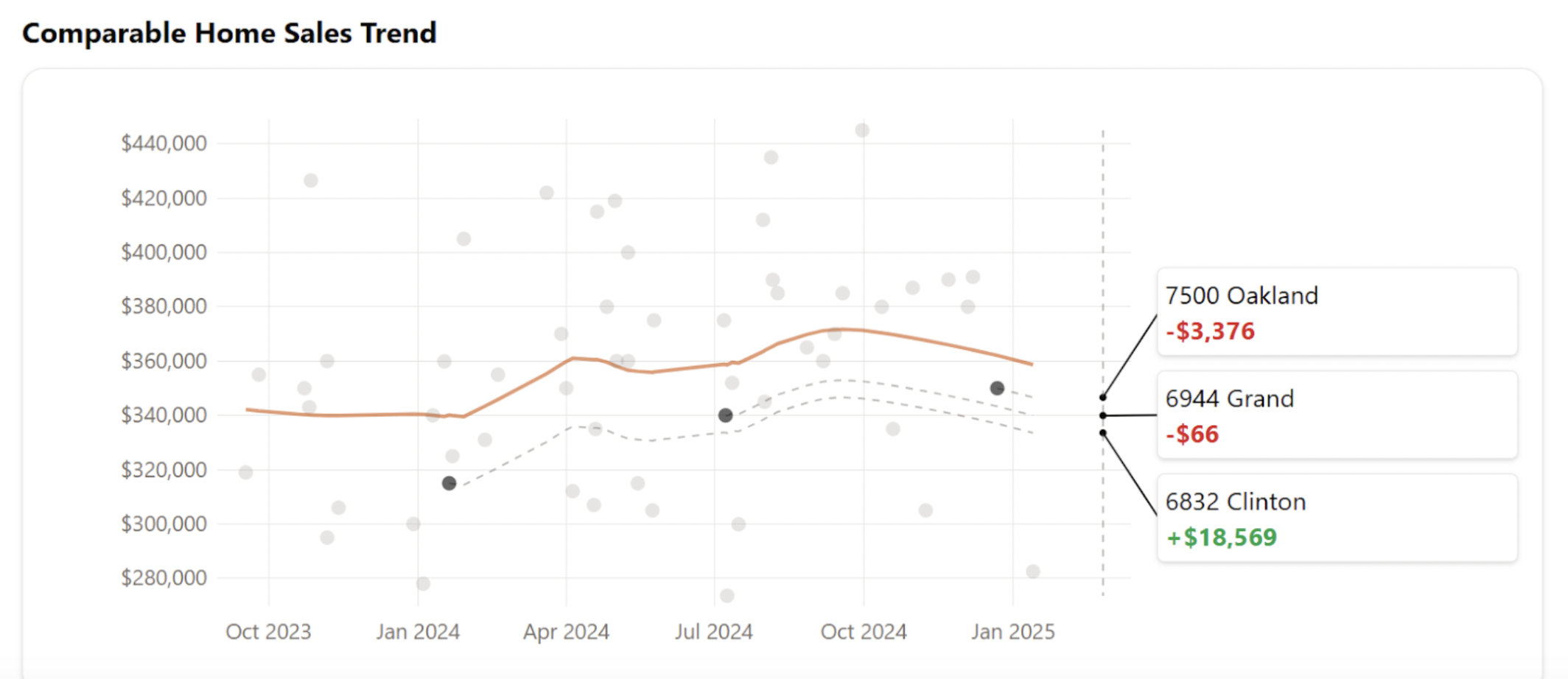

Fannie Mae’s new requirement prompted the development of responsive methods of calculating market conditions adjustments. In this example from Teeba (teeba-calculator.com), a scatter chart shows the change in price over time. Locally weighted regression guards against exaggerated change toward the effective date of the appraisal.

Comparable sales follow market changes seen in the trend line. This shows the vertical (y) axis change of individual comparables from contract date to the effective date of the appraisal. In this case, 7500 Oakland indicates a y axis change of negative $3,400. 6944 Grand is so close to the effective date that no market change adjustment is necessary. 6832 Clinton from the prior frigid winter rides the trend line through three changes in direction and arrives at the effective date with a net positive market change of $18,600. Rather than confusion of positive and negative rates of change, this method shows a simple market change adjustment.

Embracing Change: Challenges and Opportunities

The shift from traditional methods like prorated annual change and polynomial trend lines is a challenge. There are several options on the market, from data science courses to web applications.

A common challenge for all methods of measuring market change is finding sufficient data. There’s always a trade-off between the relevance of market change data and the amount of data required to make credible analysis possible.

Sale and resale of properties seldom work in a seasonal market because such pairs are seldom found, especially when matching the seasonal effect. A sale from January and resale in June does not show a rate of change that is relevant to a property being appraised in October.

The S&P CoreLogic Case-Schiller U.S. National Home Price Index is widely used to show changes in the housing market but may not be relevant to your local market. The Federal Housing Finance Agency operates the HPI (house price calculator) that works at the MSA level. The disclaimer states:

“When using the FHFA House Price Calculator, please note that it does not project the actual value of any particular house. Rather, it projects what a given house purchased at a point in time would be worth today if it appreciated at the average appreciation rate of all homes in the area. The actual value of any house will depend on the local real estate market, house condition and age, home improvements made and needed, and many other factors. Consult a qualified real estate appraiser in your area to obtain a professional estimate of the current value of your home.”

On the other hand, there are opportunities for appraisers who master a method that accurately shows market change throughout the year in their market. By embracing these innovations, appraisers can provide clients with more accurate and defensible valuations. This is particularly important in seasonal markets.

Conclusion

The evolution of market change adjustment methodologies marks a turning point in the appraisal profession. What began as a reliance on grouped data analysis and polynomial trends is transforming into a more sophisticated approach that reveals market complexities that have been hidden from view. As Fannie Mae’s guidance demonstrates, annualized rates no longer suffice in a world where market conditions vary widely within a single year.

For appraisers, the challenge is clear: adapt to these changes or risk falling behind. By selecting and mastering tools that work in your market, appraisers remain compliant and position themselves as experts for private work. As markets continue to change, so must the methods we use to understand them. The future of appraisal lies in embracing change — and in doing so, ensuring that the profession remains as dynamic and adaptable as the markets it serves.

Share this article

Written by : Scott Cullen

Scott Cullen is a Certified Residential Appraiser in Eagan, MN. He has mentored four trainees who became Certified Residential Appraisers, completed more than 6,000 appraisal assignments since 1999, and co-founded SolomonAppraisal.com, an app used by U.S.- and Canada-based working appraisers, including several USPAP instructors and review appraisers. He has written a CE course and several professional development classes for Appraiser eLearning. Reach Scott at scullen2@comcast.net